NHC +5.05% reported full year results today that were largely inline with expectations;

- FY25 revenue was flat YoY at $1.8bn, inline with consensus.

- EPS of A$0.50 (consensus A$0.49), Profit slipped as softer coal prices outweighed higher production.

- NPAT fell 7.7% to $439m

The board declared a 15c fully franked dividend (down from 22c) and reintroduced a Dividend Reinvestment Plan, a move that excited some. Costs fell 8% y/y, with management confident they can hold the line if production targets are met.

- Growth remains organic, with Bengalla and New Acland the key levers—though the 15Mtpa goal has slipped to FY29 due to logistics.

Overall, not a blowout, but a solid, capital-disciplined update. The combination of a clean beat at the EPS line, a fully franked payout, and DRP sweetener was enough to push shares higher today.

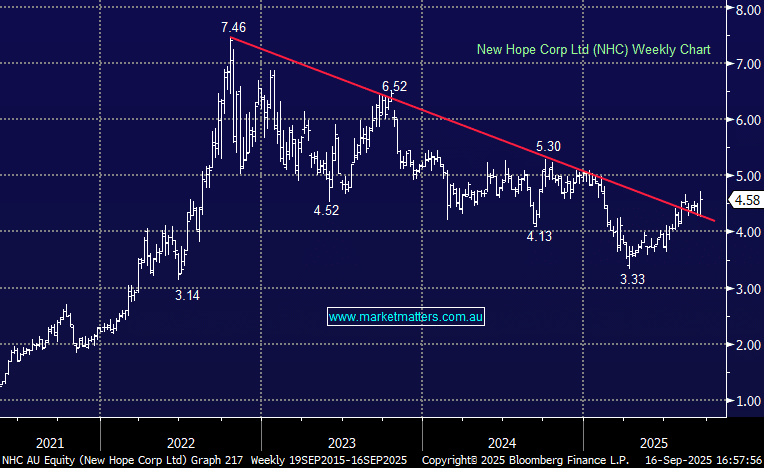

MM remains long & bullish NHC for income

Add To Hit List