MQG has lagged the “Big Four” banks even while the US investment banks forged ahead primarily because they’ve had a string of weaker updates. However, this week their third-quarter trading update was in line with expectations, with improving momentum across its markets-facing businesses. In line with US peers, guidance for Commodities & Global Markets (CGM) has improved, with management now expecting income growth rather than flat performance, supported by stronger activity across commodities and asset finance. Markets-facing businesses rose more than 25% for the period, a notable positive given the volatile global trading backdrop.

MQG banking division is producing an impressive 13% ROE, well ahead of the Big Four’s average 10.5%. While its growth in home loans and retail deposits is disrupting the banking market, ongoing growth may become harder as its market share increases. One question is whether MQG’s strong growth across this area is a function of its technology &/or marketing, or thanks to regulatory advantages, as they don’t need to hold the same level of capital as the majors – perhaps in time they may lose this advantage as their success continues.

- We prefer the big four banks to MQG at this stage, although it is a relatively close call.

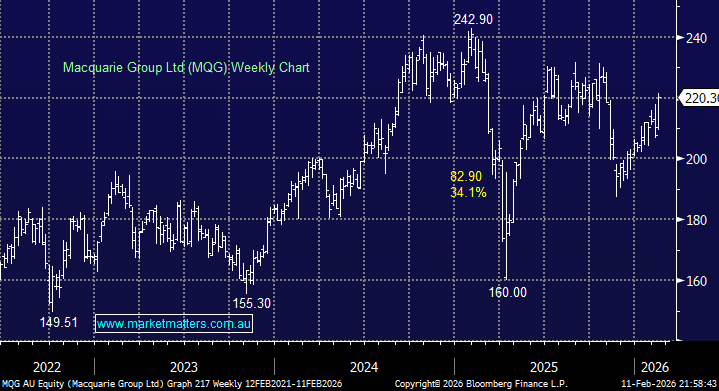

MM is neutral towards MQG around $220

Add To Hit List