Hi Guys,

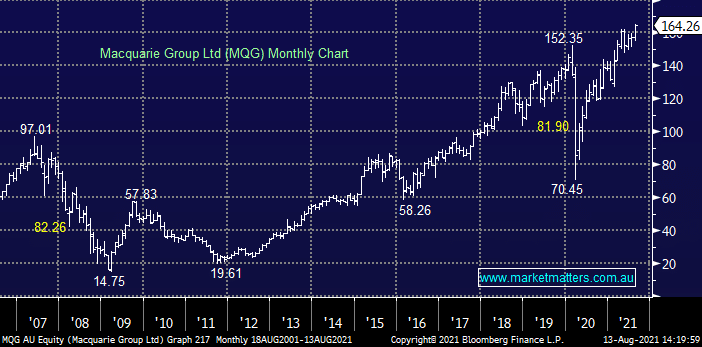

MQG has broken out to new highs this week in line with the general strong tone towards both Australian and US banks. In line with MM’s general view towards today’s market we like MQG but would be reticent to chase into current strength.

Moving onto their new hybrid offer, the Macquarie Bank Capital Notes 3 is set to raise $400 million and will list under code MBLPD. It is a typical tier 1 hybrid security with all the usual conditions. The margin will be set at 2.9% p.a. above the 90-day bank bill swap rate so pays circa 3% pa grossed for franking. The margin of 2.9% is the same rate as the last Macquarie hybrid issued in February 2021 which is currently trading on a margin of ~2.8%.

In short, the new note is reasonable relative to the current market however, we’re not participating in this offer simply from a risk / reward perspective – we prefer the major bank hybrids given their capital positions, for example, the NABPH is trading on 2.71% over bank bills but is more than 19bps lower risk than MQG. See the link below for a Hybrid Rate Sheet from my Income Team at Shaw.

Hybrid Rate Sheet