Macquarie Group shares edged higher today after reporting a third-quarter trading update that was inline with expectations, with improving momentum across its markets-facing businesses.

Guidance for Commodities & Global Markets (CGM) has improved, now pointing to income growth rather than flat outcomes, reflecting stronger activity in commodities and asset finance.

Markets-facing businesses were up more than 25% on the prior corresponding period, a clear positive in what has been a choppy backdrop for global trading conditions. The stronger operating outlook is being partly offset by a higher-than-expected FY26 tax rate of ~31%, UBS estimates that implies an additional ~$250m tax bill, or a 5.5% hit to projected cash profit versus its prior forecasts.

Across divisions, commentary remained constructive. Banking and Financial Services continues to grow deposits and lending above system, despite ongoing margin pressure, while Macquarie Capital benefited from asset realisations and the ongoing build-out of its private credit portfolio.

Macquarie trades on around 17.5x forward earnings, inline with historical averages. While higher tax expense is a headwind, the underlying operating momentum remains intact.

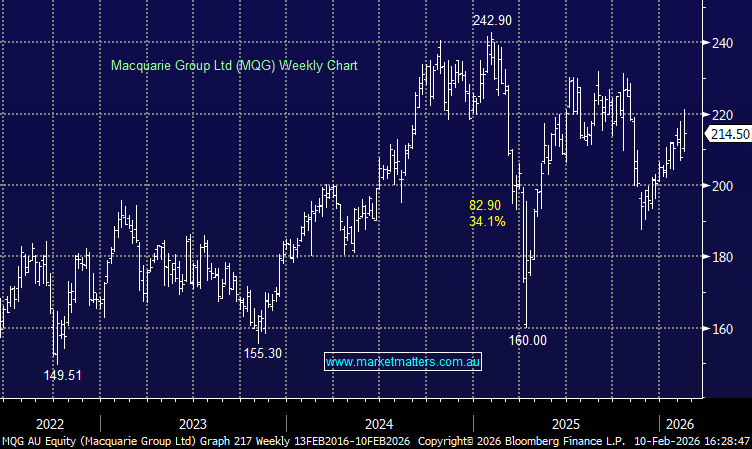

MM remains neutral MQG ~$215

Add To Hit List