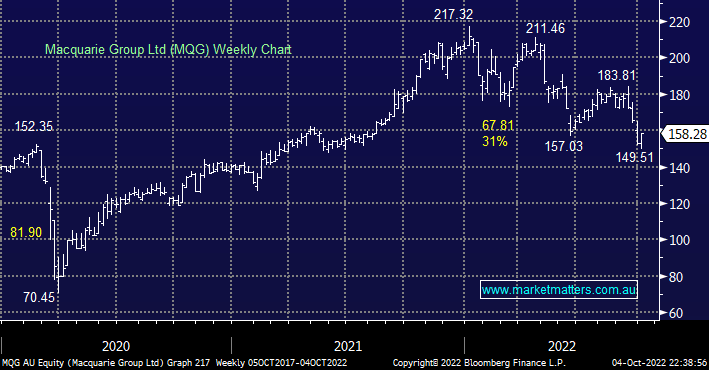

Investment bank MQG has tumbled over 30% in sync but the magnified manner to the local market which has declined less than 16% i.e. cementing its position as a classic high beta stock. Over recent weeks we have been considering buying NAB, which resides in our Hitlist, but considering the comparative pullback by MQG we now believe it offers better value – they both trade ex-dividend in November with Macquarie forecast to pay $2.75 part franked putting it on a yield of around 4.1%.

- MQG is currently trading on 14.6x earnings which is below its long-term average and PE relative to the market.

- Diversification of the business aids resilience of the group’s earnings base but a recession would clearly hurt this as client activity would slow.

- Encouragingly, Macquarie continues to dominate the household deposit market, growing +7.6% in August compared to the major’s +0.4% month on month and the regional’s +1.4%.

We believe MQG is a great vehicle to increase our exposure to a reduction of economic concerns with our initial target ~$180, or 15% higher. Recent weakness in the market caused by hawkish central banks has seen some analysts pare back their view for MQG with 2 strong buys, 7 buys, 3 holds and 2 sells.

MM is bullish MQG and looking to increase our position~$160

Add To Hit List