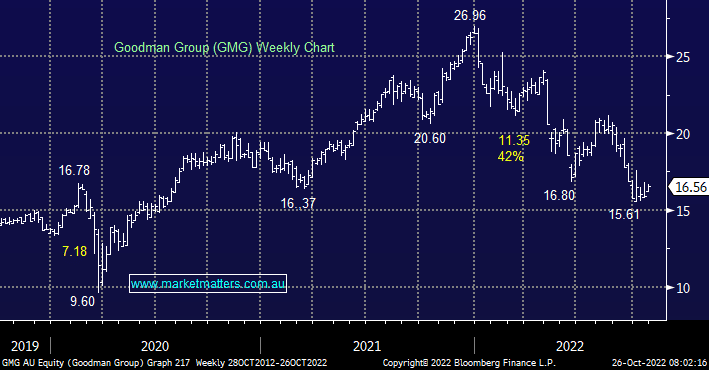

In August this integrated property company reported FY22 earnings up 24% on FY21 which was a strong result plus they talked to a strong development pipeline for the year ahead. Management guided to 11% growth at the EPS line which is slightly below where the market was positioned for FY23, however, they do have a habit of under-promising, and over-delivering. We simply feel that GMG’s share price decline of 40% this year is well overdone for this quality business.

- GMG has certainly experienced a year to forget so far but we feel it’s a quality business that is offering excellent value below $17

- We lightened our holding in August as the stock surged through $20, we believe the elastic band is now equally stretched on the downside.

MM is high conviction on GMG

Add To Hit List