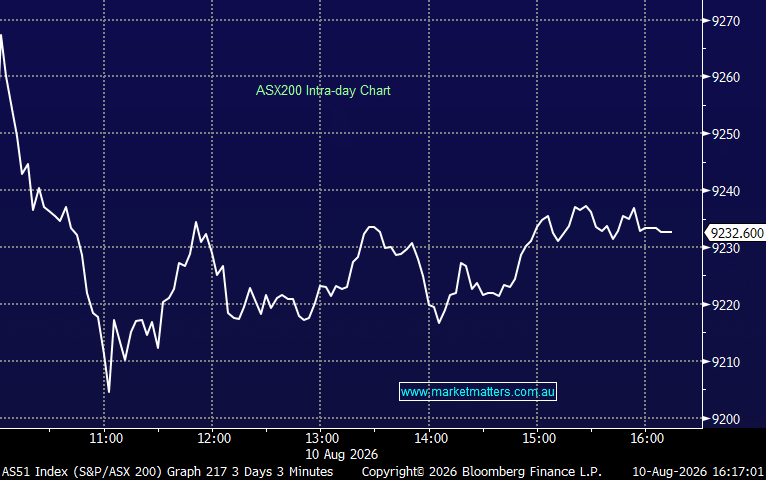

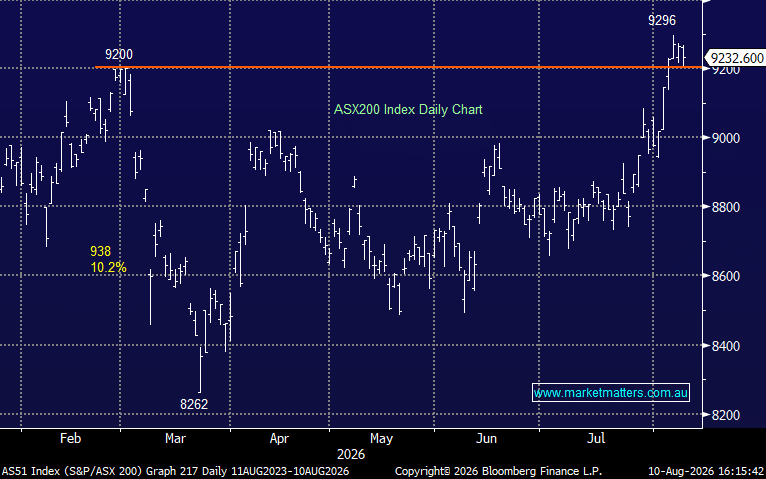

The ASX200 market slipped lower throughout the shortened week, finally closing down -2%, with a very heavy Resources Sector dragging the index lower. The EOFY is only a fortnight away, with volatility likely to lift on the stock level, and history tells us that’s not great for the underperformers. Year to date, the Materials Sector is down -11.7%, making it a prime target for some tax loss selling.

- The SPI Futures are pointing to a drop of 0.2% this morning, with BHP’s 15c fall in the US not helping proceedings.

MM is neutral towards the ASX200

Add To Hit List

US equities remained firm through 2024 as the doubters became increasingly vocal. Now, their main rhetoric is that it’s a two-stock rally (Apple and Nvidia), but who is to say another large-cap won’t join the party? The trend is up, and surprises usually unfold with the trend. Investment heavyweight Goldman Sachs has just lifted its S&P500 target to 5600 from 5200, a similar move to UBS’s recent bullish tweak as Wall Street capitulates in the face of a rising market. Goldman’s reasoning for the upgrade was “driven by-milder-than average negative earnings and a higher fair value P/E multiples”.

- Over the coming weeks, our ideal target for the S&P500 is ~5,500, which is now just over 1% away. Hence, we are neutral, although the bull trend remains intact.

MM is neutral towards US stocks in the short term

Add To Hit List

The Japanese Nikkei continues to follow the “MM Roadmap” through 2024, which makes it worth watching carefully due to its decent correlation to major global indices. If the Nikkei continues to follow our path, it’s a good sign for the bulls as we approach the seasonally strong month of July.

- We are targeting the Nikkei to reach new highs in 2024, or over 8% higher.

MM is cautiously bullish towards the Nikkei short-term

Add To Hit List