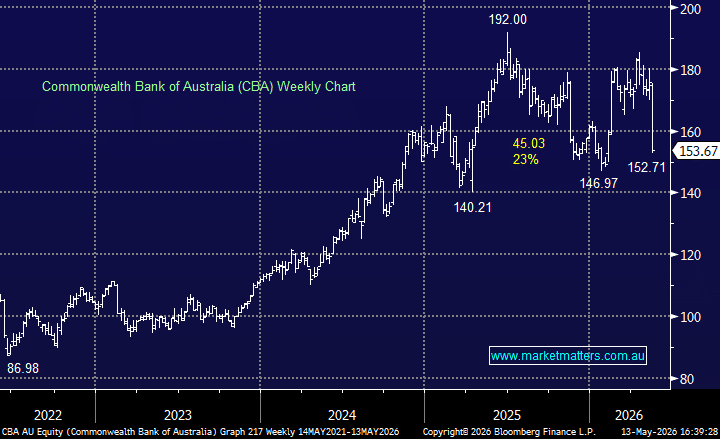

CBA –10.43%: was whacked today after its 3Q update highlighted rising provisions and a more cautious macro-outlook, amplified by concerns around negative gearing and the implications for housing credit growth.

- Unaudited cash profit: ~$2.7bn

- Loan impairment expense: $316m

- CET1 ratio: 11.6%

The result itself was broadly in line, with operating income flat and margins stable, though the market focused on the bank increasing collective provisions by $200m amid heightened economic uncertainty tied to the Middle East conflict and softer consumer conditions.

Importantly, investor mortgages have been a key earnings driver for the majors over the past decade given they typically carry higher margins than owner-occupier loans. A shift away from investor lending could pressure sector Net Interest Margins (NIMs) modestly over time, while also intensifying competition for owner-occupier flow.

While the result wasn’t disastrous operationally, the combination of elevated provisioning, softer macro sentiment and housing-related policy changes drove a sharp de-rating in the stock. Not to mention, the stock continues to trade on a significant premium to peers.

MM is neutral toward CBA

Add To Hit List