Centuria Capital Group (CNI) has moved to strengthen its balance sheet and fund the next leg of growth, announcing a $300m equity raising at $2.00 per security. The raising comprises a $200m institutional placement and a 1-for-17 entitlement offer, with around 150m new securities to be issued.

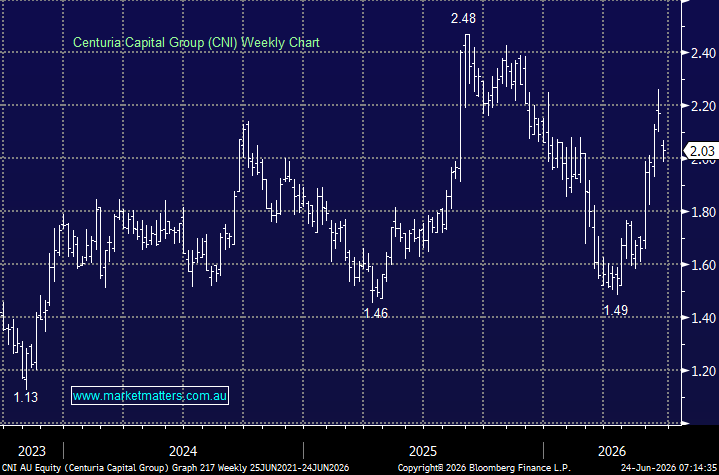

CNI had rallied sharply into the raise, helped by improving sentiment towards real estate stocks and growing interest in its ResetData platform. No doubt that strength encouraged the board to press the button now and shore up the balance sheet while capital markets were receptive. Ultimately, we think the rationale is sound. The proceeds will be used to reduce debt, strengthen the group’s funding position, and provide capacity to support ResetData’s development pipeline, which has become an increasingly important part of the Centuria investment case.

The key attraction is that the raising appears only modestly dilutive. Jefferies estimates the impact on FY27 earnings will be less than 1%, before allowing for any upside from reinvesting capital into ResetData and other growth opportunities. On its numbers, using proceeds to repay debt lifts pro-forma NTA by around 2% to $1.81 per security, while reducing operating gearing to 3% and look-through gearing to 32%. That is a better balance sheet at a time when property managers are still being judged harshly on funding risk.

ResetData remains the swing factor. By way of refresher, ResetData is Centuria’s data centre platform — essentially its push into AI/cloud-related infrastructure. In simple terms, it develops and operates modular data centre capacity for customers requiring high-performance computing power, including AI workloads. For CNI, the attraction is that it adds a higher-growth technology infrastructure angle to what has traditionally been a real estate funds management business.

The platform’s pipeline has grown to 23MW, including the addition of 10MW under heads of agreement and master services agreements. Its AI-F1 facility has 1.1MW of live capacity, currently around 33% utilised. The opportunity is clearly there, but investors should also recognise that part of the expansion pipeline remains non-binding, including 13MW due to expire at the end of June. In other words, this is not yet a fully de-risked growth component of the CNI business.

Broker views are mixed, although still broadly constructive. Jefferies retained its Buy rating and lifted its price target to $2.66, while CLSA upgraded the stock to accumulate with a $2.42 target. Others are more cautious, with Moelis moving to hold with a $2.18 target, Macquarie sitting as the most bearish on the street at underperform with a $1.88 target, and Bell Potter reducing its target to $2.00. Consensus still leans positive, with the stock offering a forecast dividend yield of around 5%+ and mid-single-digit earnings growth over the next few years.

For us, the raise is a sensible, if opportunistic, step. Management is using recent share price strength to address funding concerns and position CNI for growth, rather than waiting until capital markets become less supportive. The dilution is manageable, the balance sheet improves, and the ResetData optionality remains attractive.

- We own Centuria Capital Group in the Emerging Companies Portfolio and will continue to hold the position. We will assess the entitlement offer closer to the closing date, being Tuesday, 7 July 2026 at 5:00 pm, with new retail securities expected to quote on ASX on Tuesday, 14 July 2026.

MM remains long & bullish CNI in the Emerging Companies Portfolio

Add To Hit List