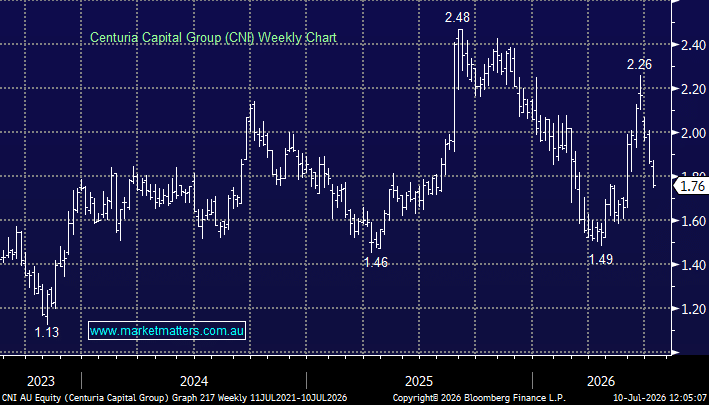

What doesn’t the market like about Centuria Capital Group (ASX: CNI) recent capital raising?

I generally don’t like buying stocks trending lower, but CNI look good value to me around $1.75. Am I missing something that the rest of the market is aware of? I would be happy to buy at these levels and top up if they fall further, but what are your thoughts on the stock as a longer term investment at these levels? Chris G. Hi MM, After not looking at CNI for some time, I just noticed that it has traded significantly under the recent equity raise price. What is the reason for this - a combination of macroeconomic and company-specific factors? Do you consider it a strong buy at these levels, particularly given the cash injection from the equity raising and reduction in gearing levels? As I have managed to slip this in before the midday cut-off, can you please answer this in this week's Weekend Report if at all possible. Thanks, Darren