NHC delivered a solid quarterly update on Monday (18th May), with production and sales volumes both ahead of the prior corresponding period, although lower realised coal prices relative to the same time last year weighed on earnings. Operations remain strong and cash generation is still healthy, but pricing has come back from the elevated levels seen over recent years.

- Group run-of-mine coal production was 4.3mt for the three months to April, up from 4.0mt in the prior corresponding period.

- Group coal sales were 3.2mt, up strongly from 2.7mt in the same quarter last year.

- Average realised sales price was $140.70/t, down from $147.50/t a year earlier.

- Underlying EBITDA was A$130.1m, compared with $155.2m in the prior corresponding period.

While prices are down YoY, NHC is still producing and selling more coal – they are controlling what they can. That is the nature of the coal cycle. Volumes matter, but commodity prices ultimately drive earnings, cash flow and dividends.

- For income investors, New Hope remains our favoured coal company on the ASX. It has historically returned a meaningful amount of cash to shareholders, and its thermal coal exposure gives it direct leverage to energy markets.

We view New Hope differently from Whitehaven. Whitehaven is increasingly skewed toward metallurgical coal and offers more growth leverage, while New Hope remains the cleaner income-style coal exposure, with greater linkage to thermal coal and power generation demand. In a world where energy security, AI-driven electricity demand and emerging-market industrialisation remain important themes, we think quality coal names can still play a role in portfolios.

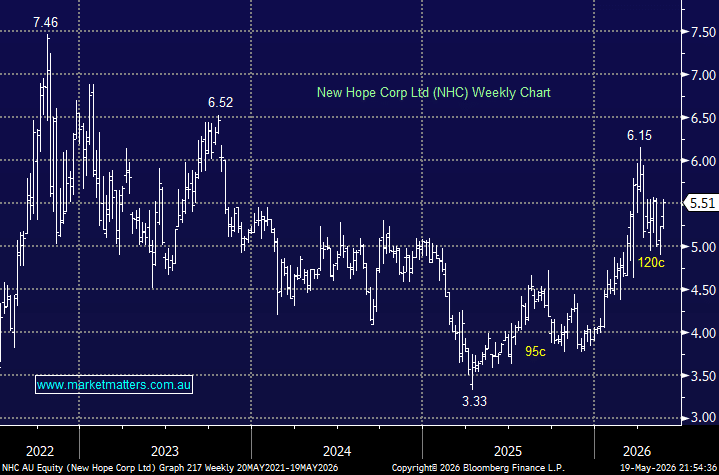

MM remains long & bullish NHC for income ~$5.50

Add To Hit List