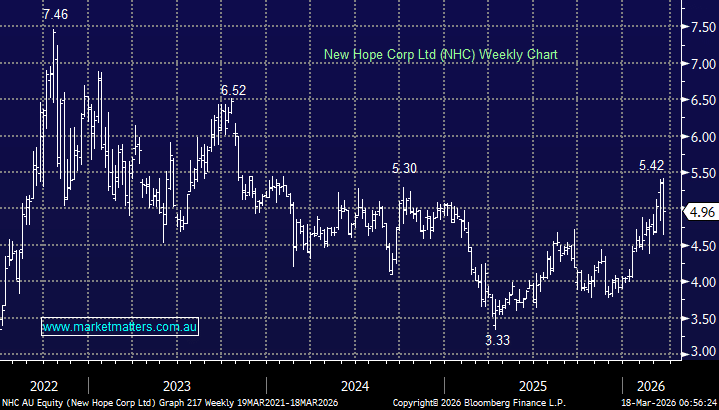

The 1H26 result from NHC wasn’t pretty on the headline numbers, and the market’s first reaction was to sell the stock down over 10%, but we argue this result was not unexpected given weakness in coal prices during the reporting period, meeting higher costs, which obviously impacts earnings. When we look through the windscreen (not the rear-view mirror), things look better.

What matters for us (as shareholders in an income-focused portfolio) is whether the business still has the cash generation, balance sheet strength, and operational momentum to keep paying a healthy dividend, and whether the next 6-12 months look “less bad” than the last. On those points, the update was better than the profit line suggests.

1H26 earnings:

- Underlying EBITDA: $214.8m (down 58.5% YoY)

- NPAT: $54.3m (down 84.0% YoY)

- Revenue: $814.4m (down 20.1% YoY)

- Interim dividend: 10.0c fully franked (payable 20 April 2026)

- Operating cash flow: $185.0m; available cash: $616.8m

The average sale price achieved was $A137.8/t (vs $A173.3/t a year earlier) and $A139.4/t including commodity and FX hedging (vs $A180.3/t). The benchmark coal price fell from an average of ~US$136/t in 1H FY25 to ~US$108/t in 1H FY26, which lines up with the realised pricing compression.

Compounding the pricing issue was higher costs, particularly at Bengalla, while the pit sequence is being re-aligned after weather disruption. Group Free on Rail (FOR) cash costs were $A60.6/t, up from $AS55.5/t, and management explicitly ties that to increased prime overburden movement, i.e., a shorter-term issue. So, prices down meaningfully, costs up modestly (but at the wrong time) and thus margins and earnings (+ dividends) took a hit.

Focusing on what the company can control is a better way to think about the result in MM’s view, and operationally, they were good. Saleable coal production was slightly higher YoY, and management was very confident that the Bengalla Mine is expected to return to the 13.4Mtpa ROM run-rate (100% basis) in 2H FY26 once the pit sequence re-alignment work is behind them. Further, the New Acland Mine continues to ramp toward ~5Mtpa, with the key next step being access to Manning Vale West pit in late calendar 2026.

More recently, coal prices have been rising, in part due to LNG disruption, which is pushing some Asian buyers toward coal as a substitute fuel. That’s obviously supportive in the near term, but we can’t lose sight of the cyclicality in the business/sector, and therefore, we should be expecting a choppier return profile from this holding. Periods of strong pricing will drive outsized dividends, interspersed with weaker halves like this one, where the dividend is weaker.

Coal prices are still the major variable, and further gains here will obviously be positive. We are bullish on coal prices in the next few years (both Thermal & Met) based on lower supply growth meeting higher demand, and this remains the key driver of our thesis. While we don’t expect a high level of capital gain from this position, we expect earnings growth to track higher production, which will feed into ongoing dividend growth – we just need to accept that dividends will remain choppier than some of our other, more stable dividend payers in the portfolio.

MM remains long & bullish NHC ~$5

Add To Hit List