- Markets @ Midday: Listen here at lunchtime or find all Market Matters Podcasts on Spotify.

- 1H26 Reporting Calendar: Spreadsheet Version Here, PDF Version Here

The ASX powered to a fresh record high today, brushing off a hotter-than-expected inflation print as investors leaned into a sharp rebound in technology stocks and a blockbuster earnings response from several companies.

The ASX200 closed at 9,128, marking its highest ever closing level, with gains broad-based across tech, materials and defensives. The move was all about earnings momentum, which came through in many of today’s updates.

- The ASX200 rallied +105pts/+1.17% to close at 9128.

- IT (+5.88%), Staples (+5.67%) and Materials (+2.68%) had a day in the sun

- Communications (-1.47%), Utilities (-0.70%) and Consumer Discretionary (-0.38%) weighed.

- A rally in US tech set the tone overnight after AI developer Anthropic downplayed fears that AI would “replace” existing software, helping ease recent valuation jitters.

- Australian CPI (3.8% YoY) came in a touch hot, but investors largely looked through it, with most attention now on May rather than March for the next potential RBA move.

- Woolworths Group (WOW) +13.0% had its largest one-day gain in’ history. 1H EBIT of $1.66bn beat consensus by ~6%, driven by a sharp turnaround at Big W and better-than-expected execution in Australian Food. Importantly, early 2H trading showed sales momentum accelerating to ~5.8

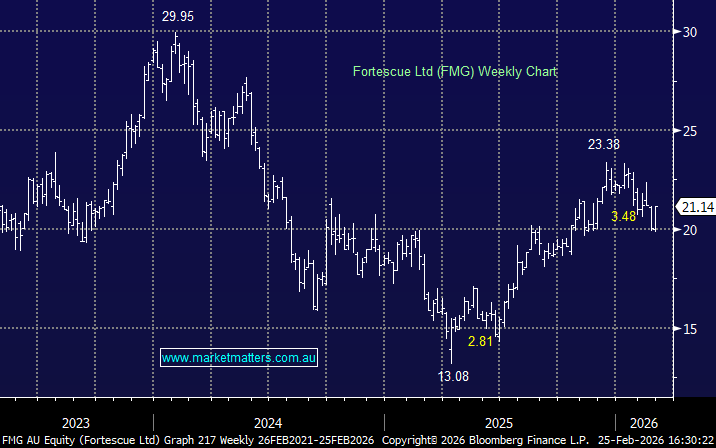

- BHP Group (BHP) +3.2% closed at a fresh all-time high as iron ore sentiment improved and Fortescue’s result reinforced confidence in sector cashflows.

- Fortescue (FMG) +4.7% posted a better interim dividend of 62¢ following a 23% jump in 1H profit.

- WiseTech Global (WTC) +11.1% reported inline with expectations and announced up to 2,000 job cuts over two years

- Xero (XRO) +5.5% benefited from the broader global tech rebound, with sentiment helped by easing fears that AI represents an existential threat to incumbent software platforms.

- NextDC (NXT) +5.4% rallied alongside the AI infrastructure complex as investors rotated back into structural growth exposures.

- DroneShield (DRO) +12.6% reported revenue up 276% to $216.5m and a small net profit, reflecting accelerating global demand for counter-drone solutions.

- Tabcorp Holdings (TAH) +23.5% enjoyed a sizeable relief rally after 1H EBITDA of $217m beat consensus by ~11%. Cost control was a key positive, and the result eased balance-sheet concerns that had weighed heavily on the stock.

- Domino’s Pizza (DMP) −11.1% was hit after cutting its interim dividend to 25¢ (from 55.5¢ last year), alongside commentary pointing to softer same-store sales. Margin pressure and execution risk remain front and center.

- Flight Centre (FLT) −3.2% fell after they reaffirmed FY profit guidance of $315–350m, implying ~15% growth, but the market was hoping for upside. With the stock already pricing in a solid travel recovery, “no upgrade” was enough to disappoint.

- Iress (IRE) +9.6% continued momentum from restructuring efforts, with management guiding to 15–24% underlying profit growth next year.

- Accent Group (AX1) +19.9% reported 1H EBIT broadly in line, but revenue up 5.3% and a dividend beat drove a sharp rerating. Early traction from Sports Direct stores added confidence to the growth outlook despite margin pressure from FX.

- Siteminder (SDR) +10.5% was higher with a largely inline result which met a share price that has been smashed of late.

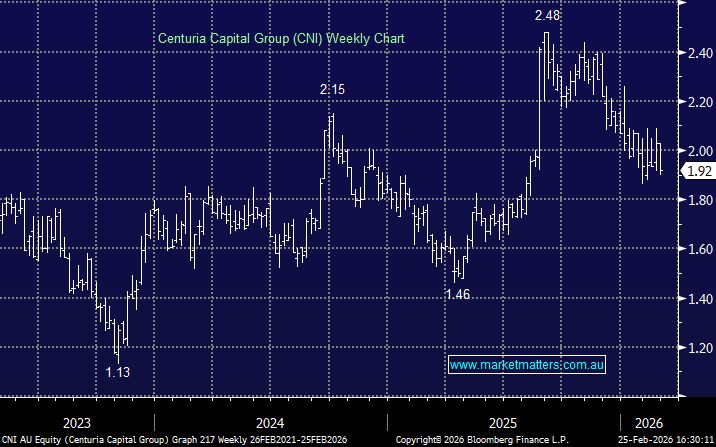

- Centuria Capital (CNI) -0.8% was lower despite marginally increasing full year guidance.

- Gold prices added $US47/oz during our time zone, trading US$5191/oz

- Iron ore rallied 2% to trade $US98.65/mt around our close

- Asian markets were sold, with China +0.6%, Hong Kong up the same and Japan added +2%.

- US futures are trading mildly higher across the board.