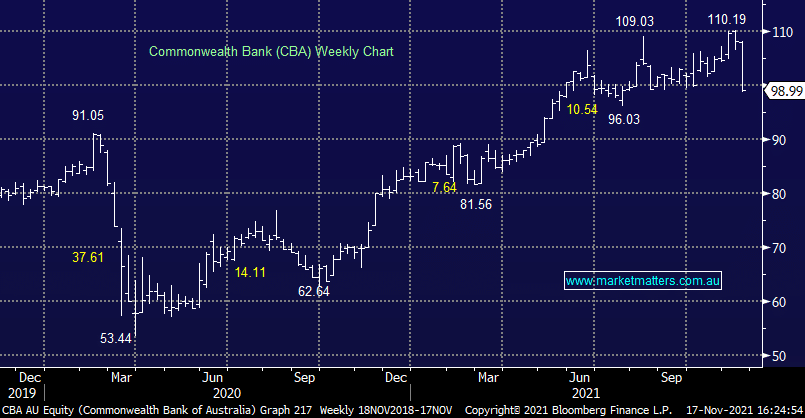

CBA -8.07%: Not often we see CBA down ~8% in a session taking a whopping 45 points from the index, however today was one of those rare days as a weaker than expected 1Q trading update and a very bullish share price leading into it broke the camel’s back.

- 1Q cash earnings of $2.2bn implies FY cash earnings of ~$8.8bn, which was ~4% below current market consensus of $9.12bn for the year

- They talked to margin pressure at the FY21 results in August and todays update sang a similar tune, in addition to higher liquid asset balances, there is increasing home loan price competition + customers (me included) are switching to lower margin fixed rate loans, plus of course the issue’s created by historically low interest rates.

- The key takeaway for MM is that even CBA’s strong franchise is not immune from the elevated margin pressures which are a result of low rates – remember, as MM has written numerous times, banks borrow short and lend long so the rise in short term rates relative to longer term rates (i.e. a flattening of the yield curve) creates an issue.

In the last 2 weeks we’ve had CFO’s from NAB & Westpac in, and all banks are saying similar things. Economic momentum is strong, however lower low rates are an issue. At MM we think rates will go higher over time and this margin pressure should subside.

We remain bullish CBA & see weakness under $100 as a buying opportunity

Add To Hit List