HomeReportsWhat Matters Today: Can the Australian “Big Banks”…

The ASX200 surged over 100 points on Monday, taking a positive lead after President Trump paused import duties on various consumer electronics. However, he warned markets on Sunday that tariffs are still coming in a social media post shortly after he finished his Sunday golf game: “NOBODY is getting off the hook”.

A slightly shorter report today as we take a deep breath after our busiest day of the year. As the saying goes, there are two certainties in life: “death and taxes”. At MM, we see it big time with investors taking out subscriptions ahead of the EOFY, a great win-win in our opinion.

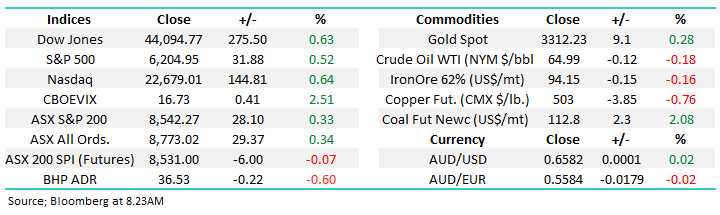

A solid final trading session for the financial year was underpinned by strength in the banks early after their U.S counterparts passed financial regulator stress testing with flying colours overnight, though it wasn’t to last with the move reversing through the session.

The most recognised equity index in the world, the US S&P 500, posted new all-time highs on Friday, leaving many fund managers and retail investors apprehensive about chasing the rally into the second half of 2025.

The ASX200 finished the week up just +0.1% after Friday's sharp, almost 100-point reversal lower from early highs, led by the banks, taking the index back towards the 8500 level. However, under the hood, not everyone danced as one, with eight of the mainboards' eleven sectors retreating, led by energy and utilities, while the advances by the heavyweight financial and resources were enough to ensure the index closed positive, albeit just:

The day kicked off with a promising +50pt open though it was short-lived as a steady rotation from the banks to resources swept through the market after a supposed resolution to US-China trade negotiations was reached triggering a –90pt swing from start to finish as we closed at the low of the day.

The ASX 200 experienced another quiet session on Thursday as the market followed the choppy consolidation, with an upside bias, that we expected at the start of the month.

A very quiet session for Aussie stocks today, though the recent trend continued with buying of weakness, although the dip was only small this morning. Xero (XRO) came back online post cap raise, down ~9% early but saw strong buying during the session to recover 50% of its loses.

The ASX200 struggled to make any meaningful headway on Wednesday, even after the Dow closed up over 500 points and we received a particularly market-friendly inflation print.

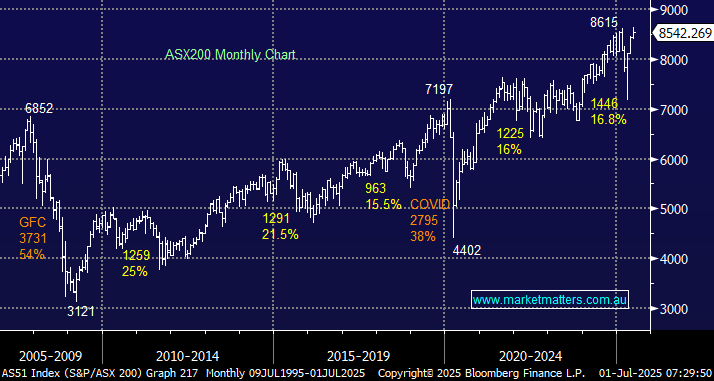

The market held on to yesterdays rally today, finishing flat, as strength continued in the banks while the miners lagged as we approach the EOFY i.e. the trends that have persisted in FY25 are extending, however, what comes in FY26 is now firmly on our radar. While it’s hard to see anyone selling CBA before the 30th June and wearing a big tax bill, CBA’s +50% gain this year (relative to its ~4% earnings growth) pushing it up to a ~12% index weight in the ASX 200 is simply extraordinary. They say trees don’t grow to the sky, but CBA is certainly having a good crack, pushing its valuation to ~29x and yield down to 2.5%, closing today at a new record of $191.40!

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

Verication email sent.

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

!

Invalid One Time Password

Please check you entered the correct info, please also note there is a 10minute time limit on the One Time Passcode

To reset your password, enter your email address

A link to create a new password will be sent to the email address you have registered to your account.