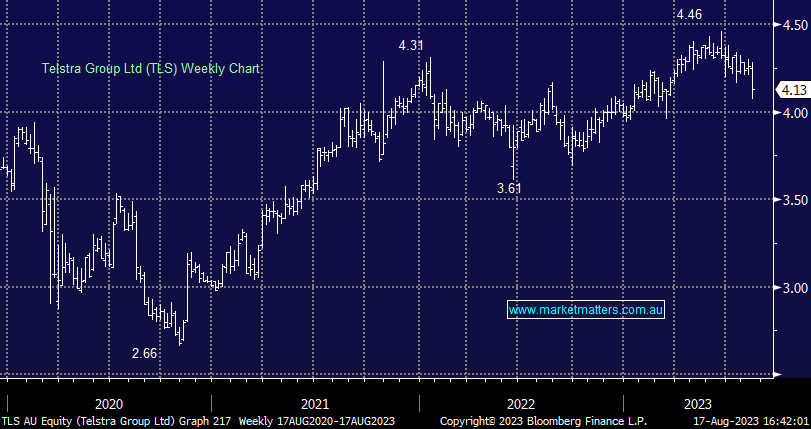

TLS -2.82%: FY23 results out today for the 10th largest company on the ASX, booking revenue of $23.24bn inline with consensus, EBITDA of $7.86bn (inline) and the all-important dividend as expected at 17cps (FY). They guided FY24 revenue of $22.8-24.8bn (mkt was $23.9bn) & underlying EBITDA of $8.2-8.4bn (mkt was $8.36bn) – all pretty much inline with existing expectations, so why the drop in the shares? 1. They poured some cold water over the near-term spinout of infrastructure & 2. Some cost pressure was obvious in the result.

- A solid result, the only real surprise was commentary around infrastructure assets being retained near term, which is understandable given the pricing environment has deteriorated.

- Consensus dividend for FY24 is 18c, rising to 19c in FY25.

MM remains a holder of TLS in the Income Portfolio

Add To Hit List