It’s straightforward to comprehend why we expect TLS to be a beneficiary from a larger Australia given it’s leverage to the population over the longer term. While short term headwinds have emerged, with more aggressive rival Aussie Broadband (ABB) which is held in our Emerging Companies Portfolio stealing market share, we do expect Telstra to receive it’s fair share of a growing population while maintaining its premium price point over competitors due to its super-network coverage and reliability. A growth than say ABB, but growth none-the-less.

- We like the risk/reward toward TLS following its recent 14% pullback.

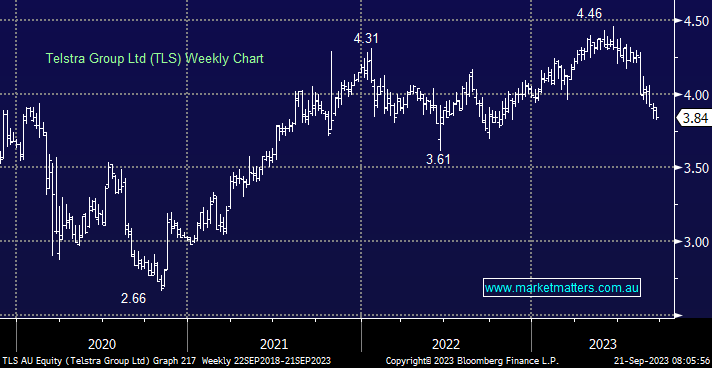

MM likes TLS under $4

Add To Hit List