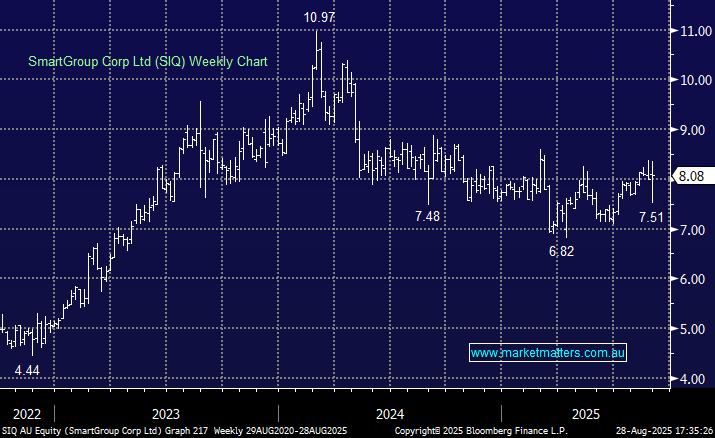

SIQ +0.5%: A decent 1H25 result with their earnings number showing they are on track to meet full-year estimates, though the revenue line was a bit soft – all things considered a good outcome given the shares were down ~7% in early trade; the rebound showing a strong appetite for quality income stocks in this market.

- Revenue of $159.1mn, +7.2% y/y missed estimates of $164.7mn

- Net income $38.1mn, +11% y/y

- Interim dividend of 19.5cps declared

SIQ is targeting EBITDA margins in the mid-40s by 2027, supported by software investment of A$11–13mn in 2025 that will streamline their distribution and sales pipeline. Demand for novated leasing remains strong, with July orders and settlements steady on last year. The business remains in good shape – momentum will build with the backdrop of a few more rate cuts.

MM remains long and bullish SIQ

Add To Hit List