Hi Chris,

Higher volumes are indeed a positive, however looking forward, the outlook for new vehicle sales and therefore new leases is less positive. The spread between new and used car prices are widening again, making 2nd hand vehicles incrementally more appealing. Interest rates have also appreciated removing another tailwind. If one can actually reduce monthly repayments via a new car purchase due to lower rates on leasing, this incentivises a change, particularly when 2nd hand car prices were so strong. That is clearly no longer the case.

Thirdly, household savings rates were very high coming out of the pandemic however these have now reverted back to levels seen prior to the pandemic. We also have ~20% of all mortgages currently on fixed rates of around 2% or better rolling off in 2023, reducing purchasing power.

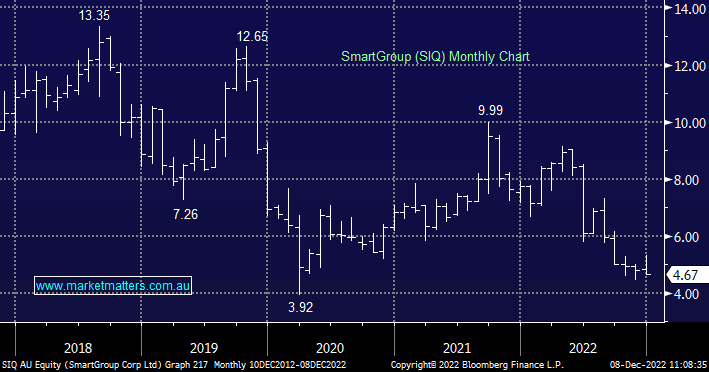

While we are not bearish on the volume of leases that will be written, and therefore not bearish on Smart Group (SIQ) given a lot of this pain is now priced in, we struggle to see a positive catalyst over the next 6-12 months, hence the removal of the stock from our hitlist, although we continue to track it closely, it’s one we do see deep value in.