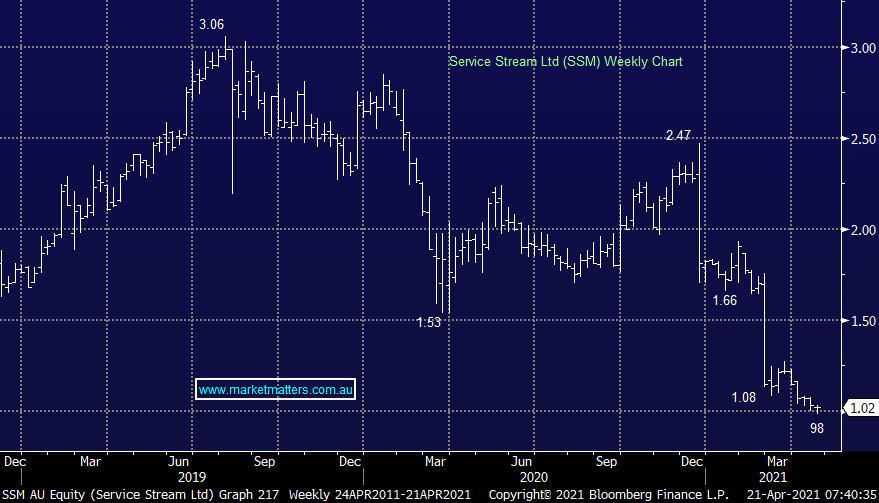

SSM has been a poor performer in the MM Income Portfolio and is down ~40% since our purchase. A string of downgrades has seen earnings expectations drop by ~30% and to make matters worse, they’ve just lost their spot in the ASX 200 (at the March rebalance). The latest update was at the end of February and they missed already lowered expectations. When revenue drops in a business like this we then see a greater impact on profit metrics as margins decline.

SSM now trades on an estimated P/E of 10.63x forward earnings while it is expected to yield ~7% fully franked, clearly strong metrics however it does come down to how earnings recover from currently depressed levels.

One potential catalyst in the near term is winning work under the NBNs upgrade program in the coming months while the team at Bells believe that M & A is also on their radar. They have a net cash position (i.e. no net debt) however there is some risk around the dividend given weakness in earnings this year. Now the stock has dipped below $1, we think too much pessimism is priced in and we are considering adding to the position, rather than cutting it.

NB: When a stock leaves the ASX 200 it is generally not a negative. If it’s an exit like SSM, it’s index weight is so low in the large cap index that many managers aligned to the ASX 200 would only own it if they wanted to. When it moves to the smaller cap indices, these managers may be forced to buy given it’s a more influential member of their benchmark, and a neutral position on the stock can actually mean owning it.

MM is now mildly bullish SSM ~$1

Add To Hit List