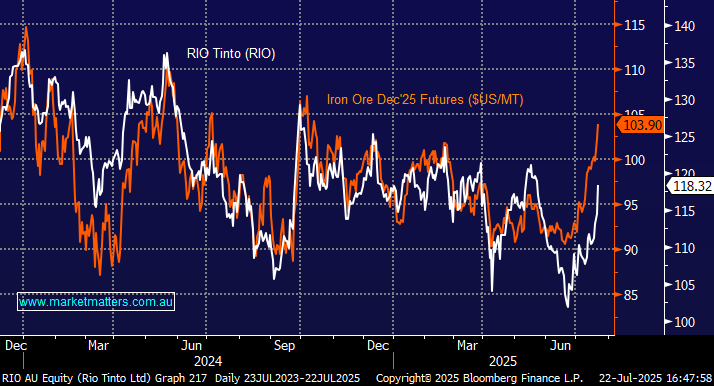

It doesn’t take much effort to see that RIO tracks the iron ore (Fe) price extremely closely. This is no surprise, as over 50% of its revenue came from the bulk commodity in FY24. RIO is a low-cost producer, with C1 cash costs in the June quarter of around $US23.50/MT, while the average realised price was $US82.50/MT, the margin being around $US59. However, on simple back-of-the-envelope calculations, the recent $US15 lift in the bulk commodity increases margins by 25% assuming, of course, levels are maintained – a whopping difference.

We’ve maintained a preference for BHP over the last year, with the “Big Australian” outperforming, albeit by only around 4% year-to-date. Today, we turned our attention to RIO given its huge Guinea mine, co-invested with China. It is due to add 5% to global supply at the end of 2025—great for RIO’s revenue stream but not necessarily for Fe prices through 2026/7. In fact, it’s indeed RIO and its Chinese partners who are largely responsible for the analyst’s negative outlook towards Fe.

As BHP evolves further towards copper and potash, Rio is actively replacing and expanding Pilbara iron ore capacity while delivering its game-changing new asset in Guinea, West Africa (Simandou). The Western Range mine is now operational and Simandou is due to come online later in 2025, with Hope Downs 2 will follow by 2027. These additions will cement RIO as the world’s second-largest Fe miner and will be very close to challenging Brazilian Vale for the top position. Hence, if Chinese demand continues to support iron ore prices, RIO will become a more interesting investment vehicle.

- We continue to see the potential risk for iron ore on the upside.

RIO reported its 2nd quarter results last week and although operationally it was mixed copper performed well (16% of revenue in FY24) and Guinean iron ore shipments, are expected in November of this year, meaning iron ore production is on track to hit prior FY26 targets. With its 5% fully franked yield, potentially conservative with iron ore around $US100/MT, the miner is attractive for growth and yield. When RIO last tested the $130 area, iron ore was trading around the $US107 area, only a few per cent above current levels. From a risk/reward perspective, we believe it’s too early to reduce exposure to iron ore, having increased our BHP position a month ago—good timing in hindsight.

- We can see RIO squeezing up towards $130 over the coming months, another 10% higher.

MM is cautiously bullish towards RIO

Add To Hit List