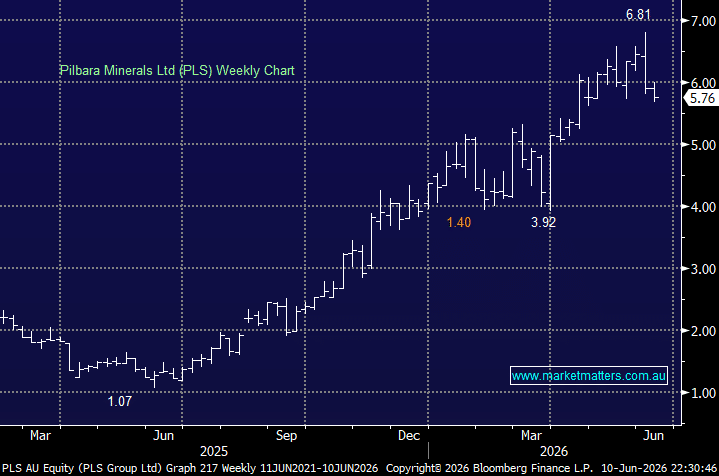

Pure lithium business Pilbara delivered a solid quarter in April, confirming its operational performance was on track, covered here. What comes next is largely down to the underlying lithium price – not unusual in the cyclical commodities space. We covered the stock in detail on April Fools Day, calling it a buy around the $5 at the time here, but after advancing another 35% to last week’s high, we have to question if the pendulum of risk has swung more in favour of caution.

With the Ngungaju restart confirmed from July, Pilbara Minerals now has a clearer pathway to higher production, supported over time by the proposed P2000 brownfield expansion and the Colina project in Brazil. The company looks well placed to meet FY26 guidance of 820–870kt, while retaining one of the lowest cost bases in the sector. Although the larger growth projects remain further out, PLS has the operational flexibility to benefit from stronger lithium prices in the near term, with consensus expecting double-digit free cash flow yields through FY27 and FY28.

- Pilbara remains our preferred stock for lithium exposure, but after such a powerful rally, the valuation now matters.

The stock is up around 470% from its June 2025 lows, which means a large part of the lithium recovery story is already reflected in the share price. We still regard PLS as one of the sector’s highest-quality operators, but it no longer screens as cheap, and from a risk-reward perspective, near-term risks are increasingly skewed to the downside.

- It may sound boring, but we are now sitting on the fence with PLS. After an almost seven-fold rally from the lows, a retest of either $4 or $7 this year would not surprise us.

MM is neutral towards PLS around $5.80

Add To Hit List