Hi Tony,

A few moving parts in the question so we’ll go through them a step at a time:

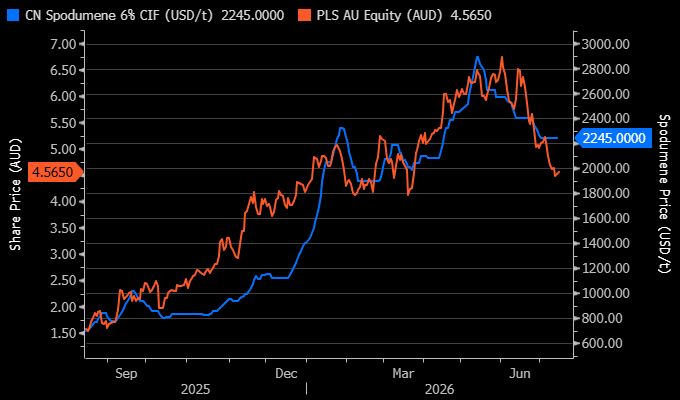

MM has been bearish towards the lithium space for the last few months but as Li retreats more than 20%, dragging the likes of heavyweight PLS Group (ASX: PLS) back towards major $4 support, ~35% off its early June high, the risk/reward is improving.

The key question remains when lithium shifts into structural deficit, with forecasts ranging from 2026–27 to 2030. We remain constructive on the long-term outlook, but after spodumene’s ~300% rally from its lows, the current consolidation was both expected and healthy. The recent correction across lithium stocks doesn’t concern us—in fact, it aligns with our view that chasing the sector after such a sharp rally was unlikely to be rewarded.

- Our preferred scenario has been for Li prices to trade in a broad US$2,000–3,000/t range through 2026 before the next leg higher – were approaching the bottom quartile now.

Hence, in general we believe it’s time to load the gun towards the space as opposed to start pressing the buy buttons.

In terms of PMT, it changed its name to PMET Resources Inc. (ASX: PMT) to reflect its evolution from a pure lithium developer to a broader critical minerals company. Its flagship Shaakichiuwaanaan Project (formerly Corvette) in Québec contains significant lithium, but also caesium, tantalum and gallium, which management believes warrant a broader corporate identity – we still like the stock below 50c from a risk/reward perspective.

However, the lithium space is volatile, and you don’t have to venture far to gain leverage to the lithium price, for example Liontown (ASX: LTR) and IGO Ltd (ASX: IGO) are both likely to gain 40-50% if lithium can return to its 2026 highs.

Out current preferences in the space at PLS & LTR in Australia, and Albemarle (ALB US) in the US – and we’ve been keeping a closer eye on them.