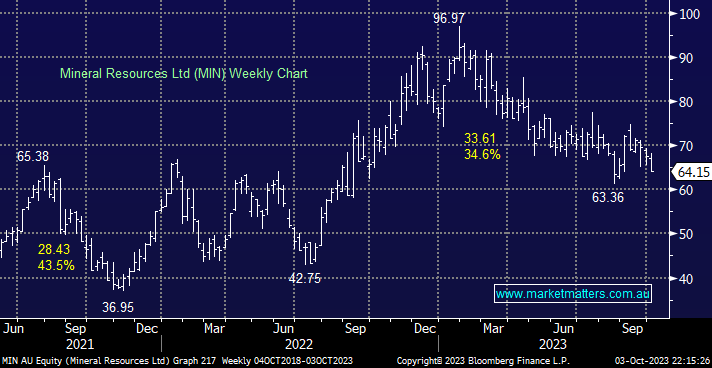

We felt MIN reported well in August, but after popping ~18% higher, the stock has been weighed down by a deteriorating broad market, including further weakness across the lithium sector, which has overshadowed relative strength across the iron ore stocks, i.e. MIN’s revenue in FY23 comprised of the eclectic mix of 44.9% iron ore, 39.6% lithium and 15.3% mining services.

- We like MIN’s lithium and iron ore combination from current levels and are considering increasing our 4% to position in our Flagship Growth Portfolio.

We bought MIN into the current pullback from its early 2023 foray on $100, but it has fallen further than expected. However, there is no change in our outlook for the company; hence we are looking where to increase our position rather than cut it.

MM is long and bullish toward MIN

Add To Hit List