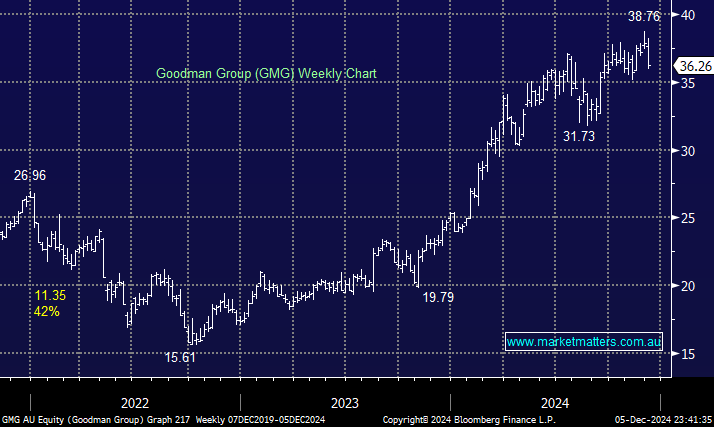

Having exited GMG above $36, this morning’s report may give us some insight as to whether the pullback into our buy area is realistic or if we’re still being too optimistic – we have already missed a couple of entry opportunities this year by being too pedantic. Rumours are Citi took a bath on this block, being too aggressive on the discount offered which is where they underwrote the transaction. Underwriting means they guarantee the seller a quoted price and take on the risk of not achieving that price when on-selling to fund managers via a bookbuild. Less than half the stock was ultimately on sold, and Citi was left with ~$1bn worth of GMG stock at a lower price than they had bought it at.

We commented at the time that the discount was slim which has proven to be the case. Further sell-downs in GMG will almost undoubtedly be exercised at a steeper discount.

- We currently see no reason to pay more for this quality company when another potential 100 million shares could be sold down in 2025.

MM likes GMG around $30-32

Add To Hit List