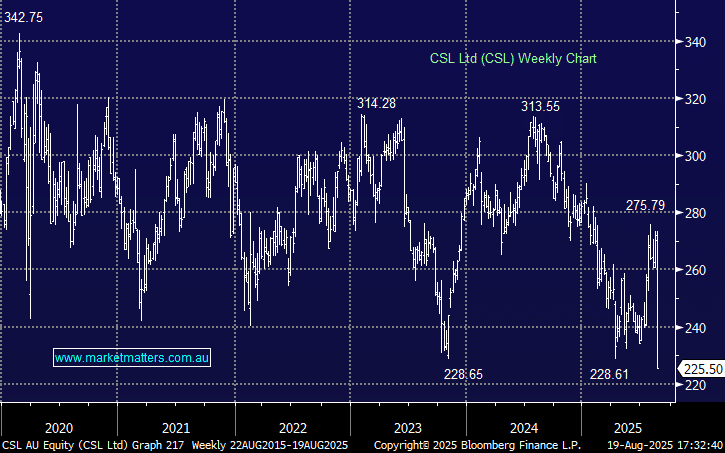

CSL –16.89%: Shares experienced their worst fall since 2008 after the FY25 result highlighted weakness in the Behring division and revealed a major strategic restructure including a spinoff of Seqirus, which has created more questions than answers.

- FY25 revenue $15.56 billion (+5.1% y/y) estimate $15.76 billion

- Net profit $3.22b (+11% y/y, vs estimate $3.17 billion

- Behring division at $11.16b (+5.2% y/y) but flat Immunoglobulin (IG) growth in 2H

Vaccine unit Seqirus will be demerged in FY26, alongside a planned A$750 million buyback, >$500 million in targeted annual cost savings by FY28, a 3000-person (15%) workforce reduction, and the closure of 22 plasma centres with one-off restructuring costs expected at $700–770 million pre-tax.

While the spinoff, buyback, and cost-out program might be attractive long-term, investors are still erring on the side of certainty – the restructure adds a level of execution risk and uncertainty to the story, and the cynic would say companies do these sorts of things to disguise underlying issues.

MM is long but now cautious toward CSL

Add To Hit List