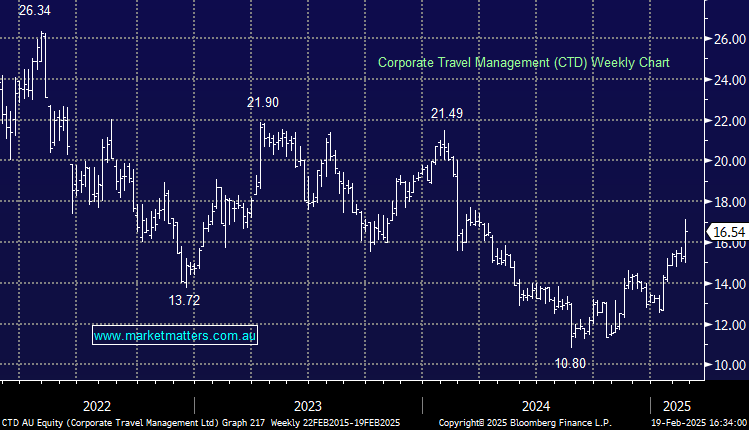

CTD +10.27%: Delivered a better than expected first half result, with earnings exceeding expectations, driven by strong revenue and profitability in both North America and Australia/New Zealand.

- 1H25 ANZ revenue of $93.8m (+16% yoy), ~8% above consensus of $86.4m

- 1H25 North America revenue of $159.9m (+6.9% yoy), in line with consensus

- 1H25 Underlying EBITDA of $77.4m (-23% yoy), 4% above consensus

- Group capex now expected to be around ~$42m in FY25, below previous indication of ~$48m

CTD new client wins are well ahead of expectations with ~$880mn of total-transaction-value (TTV) secured as at 14 February vs. expected $1.0bn for the full year. Paired with ~97% customer retention, this momentum is expected to set up a solid second half and beyond. While potential 2H25 Europe and U.K downgrades are a risk, the business is positioned so that this weakness is offset by stronger performance in other regions.

MM is cautiously bullish CTD

Add To Hit List