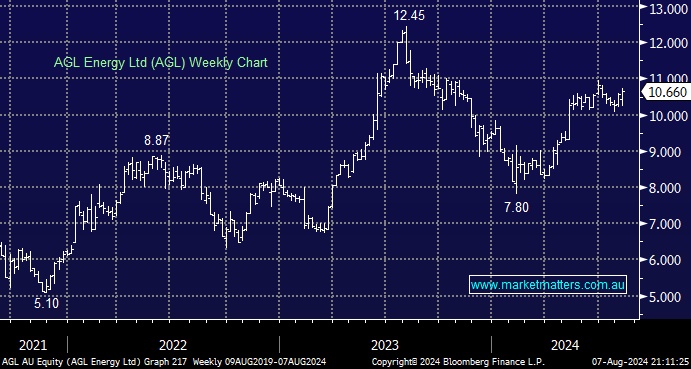

AGL has performed stoically over the last few sessions, as would be expected from a defensive utility stock. Assuming there are no nasty surprises next week, shareholders like ourselves should be rewarded with a reasonable 24cps dividend before the end of August, which will grow in the coming years. We’ve owned AGL in the Income Portfolio since early 2023, and we recently added it to the Active Growth Portfolio as we got more comfortable with its earnings outlook while navigating through a complex period. The reasons MM bought AGL most recently in May, as a high-yielding defensive play with solid and growing tailwinds from the energy transition, continue to look on point.

- We continue to initially target a retest of the $12 area, or +12% higher.

NB AGL reports next Tuesday, the 14th.

MM is long and bullish AGL

Add To Hit List