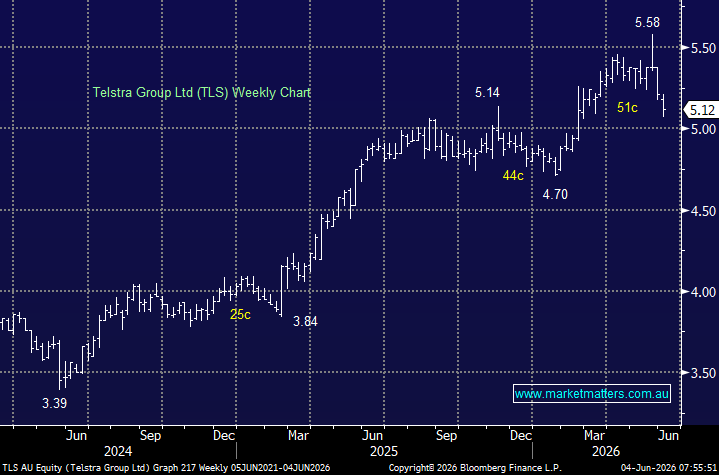

Telstra needs no introductions, and has probably frustrated most subscribers at one stage or another over recent years. We covered Telstra’s most recent report, its H1 FY26 half-year result, in February here. In a nutshell, we liked what we read but felt the stock was rich trading ~$5.50; however, that has changed following the stock’s ~10% pullback over the last 3-weeks, as monies rotated out of defensive names.

Telstra sits in an interesting position in the AI debate, not as a technology developer, but as one of the largest potential beneficiaries of AI-driven productivity on the ASX. With over 30,000 employees, millions of customer interactions daily and a nationwide network of extraordinary complexity, the efficiency opportunity is material. The T22 and T25 programs delivered a combined A$3 billion-plus in savings, but the heavy lifting was done through headcount reduction and process simplification, tools that are now largely exhausted.

What comes next is different: AI-led automation across customer service, network fault detection and back-office operations has the potential to unlock a further step-change in margins that consensus numbers may not be fully pricing in. For a business of Telstra’s scale, even modest improvements in productivity can have a meaningful impact on earnings, therefore the productivity runway here is one of the most underappreciated aspects of the Telstra investment case.

We can see this “boring defensive” outperforming over the coming years, helped by its forecasted 4.2% fully-franked yield over the coming 12-months.

- We can see TLS trading below $5 in the coming months, where we see the risk/reward returning to the Telco as its “Defensive Bid” dissipates.

MM would start to get interested in TLS below $5

Add To Hit List