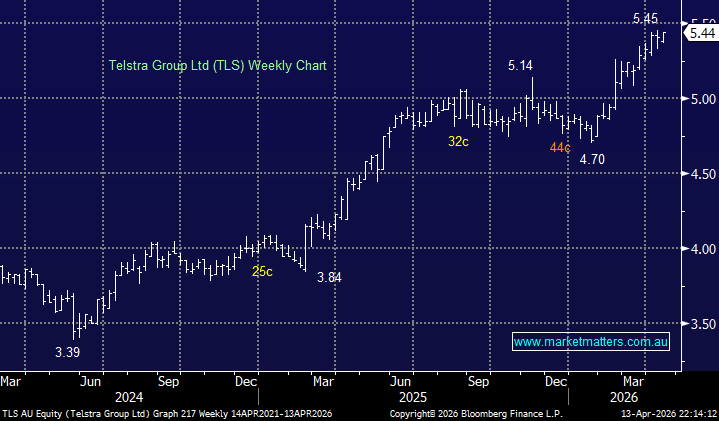

Telstra delivered a solid result in February Here which has helped push the stock towards its 10-year high although it benefitted in March from a “Defensive” bid as the Iran war saw traders and investors adopt a “risk off” approach to the market. The stock’s ~4% fully franked dividend is not as exciting as it has been in previous years, especially with the RBA in the middle of a hiking cycle.

We believe Telstra’s cost structure is perfect for further AI intervention, a sprawling network operation, millions of customer interactions annually, and a complex legacy technology stack built over decades. AI-driven customer service automation, network fault prediction, and back-office process optimisation represent a genuine multi-hundred million dollar cost reduction opportunity. TLS is already cutting costs, but the bulk of the savings to date have come from traditional restructuring rather than AI-driven process transformation. With a workforce still above 30,000, already down ~10% from last year, and one of the largest customer service operations in Australia, the AI efficiency runway ahead is still substantial.

Beyond customer service automation, TLS’s most compelling AI opportunity lies in its network. With tens of thousands of kilometres of fibre and infrastructure spanning remote Australia, the cost of reactive maintenance and unplanned outages is enormous. AI-driven predictive maintenance, identifying equipment failures before they occur and scheduling proactive repairs, could dramatically reduce expensive callouts to remote sites and cut the direct and indirect costs of outages. The second angle is real-time network optimisation, dynamically routing traffic, managing congestion, and allocating infrastructure bandwidth more efficiently as data consumption grows. At Telstra’s scale, AI that allows the business to sweat existing network assets harder before committing to new physical infrastructure is as valuable as any headcount reduction. Deferring capex while maintaining customer experience is a genuine earnings lever that the market is yet to fully price in.

- We like TLS through 2026/7 but the risk/reward isn’t as exciting after is recent defensive strength.

MM is neutral towards TLS around $5.50

Add To Hit List