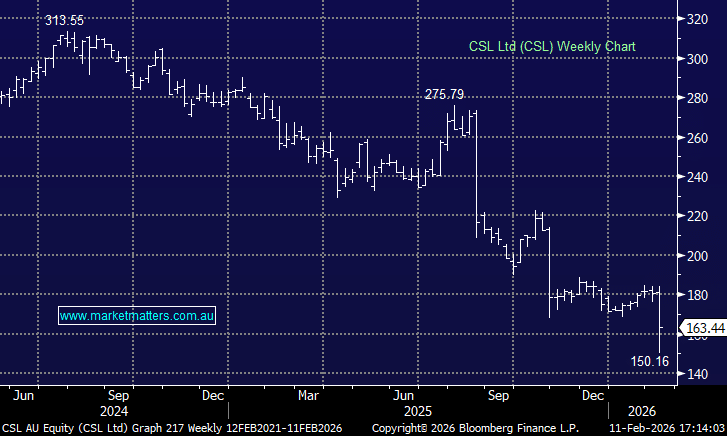

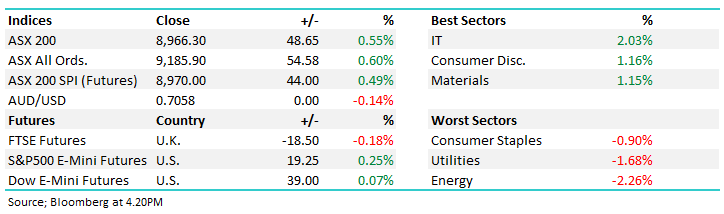

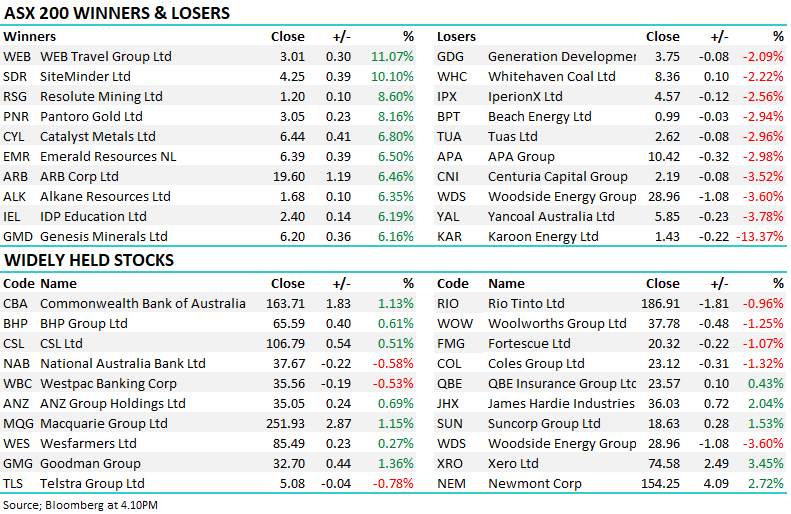

CSL -4.64%: Traded down today on a 1H miss and scepticism they’ll meet full year guidance, which they re-affirmed this morning. The stock was down ~13% at the lows before sanity prevailed and it recovered some of the very steep early decline. We covered the result this morning here, so we’ll just give some flavor around other broker’s views on the number. At MM, we don’t think the result is as bad as the market reaction implies, and this mornings brutal sell-off down to $150.16, will ultimately prove to be a low point for CSL.

- Citi: “We think there is now a very large question mark around what CSL can say to convince investors that ambitions for 2H can be realised”& The miss in first half Npata implies “mid single-digit cuts to both consensus and our estimates”

- Barrenjoey: 1H26 Npata was 3% below consensus, with “particularly weak Behring revenue” & Large misses versus consensus in IG, albumin and Kcentra revenue

- Jefferies: “Result not as bad as feared,” with Npata beating Jefferies’ estimates of $1.79 billion

- UBS: Underlying result ~3.5% lower than VA consensus largely due to higher interest and tax, with operating profit inline.

No doubt, some complexity remains here and now the uncertainty with a new CEO, however, todays result seemed to us like the nadir of bad news, and the confidence to lift the buy-back to $750m is worth noting.

MM is now looking to add to our underweight CSL position in the Growth Portfolio

Add To Hit List