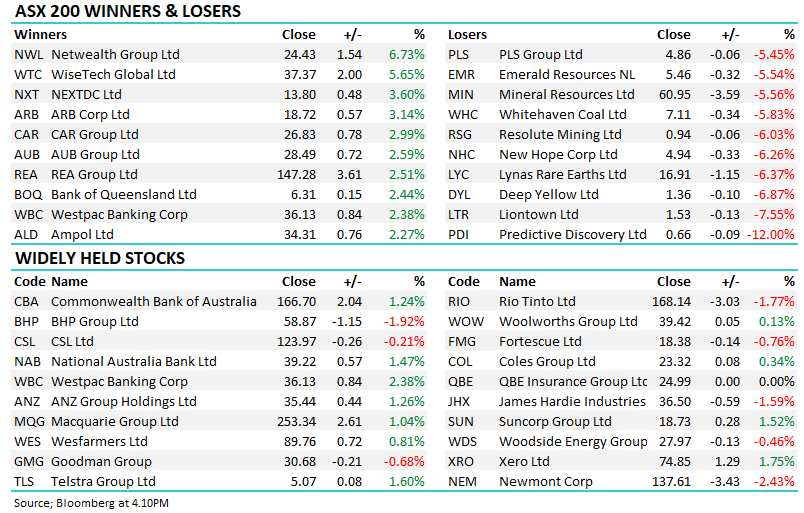

CSL -15.87: Belted today, down as much as 17% to the lowest level since 2018, after the company scrapped its 2026 target to demerge Seqirus. The reason? A sharp drop in US flu vaccination rates (-12% overall, -14% in seniors), pushing Seqirus revenues into a mid-teens decline and undermining the value case for a standalone listing.

Management stressed the separation remains the long-term plan, but they won’t proceed until market conditions allow shareholders to realise the full upside. In the meantime, Seqirus remains operationally distinct within the group while CSL pushes ahead with broader cost cuts, including a ~15% workforce reduction and $500m annualised savings.

- Guidance was cut again: FY26 revenue growth 2–3% (from 4–5%) and profit growth 4–7% (from 7–10%). That is the real sting — another downgrade in a year the stock has already fallen ~36%.

While the underlying CSL Behring plasma franchise remains world-class, today’s move feels heavily sentiment-driven with investors ‘giving up’ on one of Australia’s recent success stories.

We’d argue on ~16x, there is little growth now priced in – handy, because they aren’t delivering much!

We own the stock, acknowledging near-term pain but backing the long-duration defensive growth CSL still offers.

MM will remain patient on CSL for now

Add To Hit List