The ASX200 only slipped -0.5% last although it felt worse with some eye-catching moves on the downside especially in the influential Resources Sector e.g. BHP Group (BHP) -4.3%, RIO Tinto (RIO) -4.3%, BlueScope Steel (BSL) -6.9% and Regis Resources (RRL) -10.8%.

- No change, we are looking to buy weakness and sell strength but for now, the market doesn’t feel pessimistic enough considering where bond yields are trading.

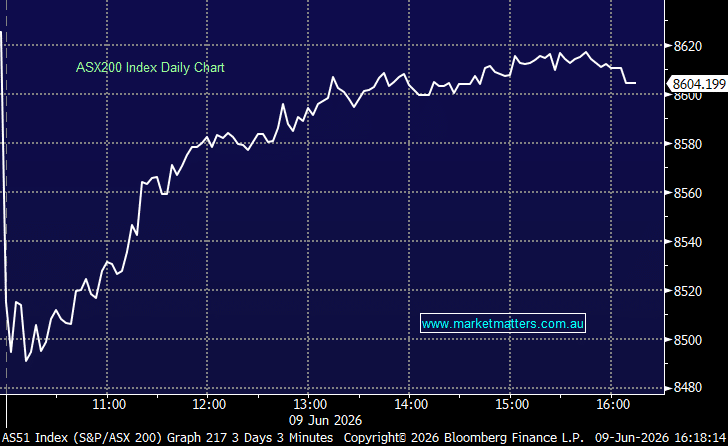

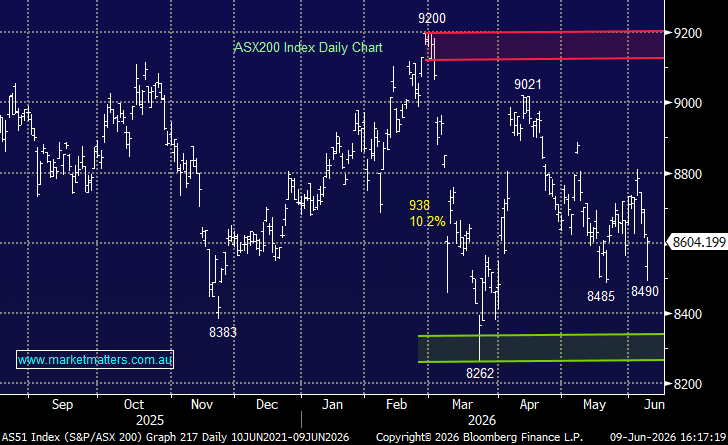

MM remains neutral towards the ASX200 around 7300

Add To Hit List

US stocks fell again on Friday after strong inflation data sent bond yields rising, we still believe the markets are in a classic rotation/choppy cycle that could last for a few more months.

- The S&P500 has been correcting its -28% fall through 2022 since mid-October with our preferred scenario the market will still eventually grind/chop back towards the 4300 area.

MM remains mildly bullish on US equities over the coming months

Add To Hit List

The tech-based NASDAQ has led the decline through February but considering that short-dated 2-year bond yields are trading at 16-year highs we believe the sector is gaining relative strength following its aggressive revaluation last year although of course, it regions vulnerable if yields surprise further on the upside.

- The growth/tech stocks are likely to recover the hardest & fastest when we finally see a reprieve to the rate fears.

MM remains mildly bullish on the Tech Sector over the coming months

Add To Hit List