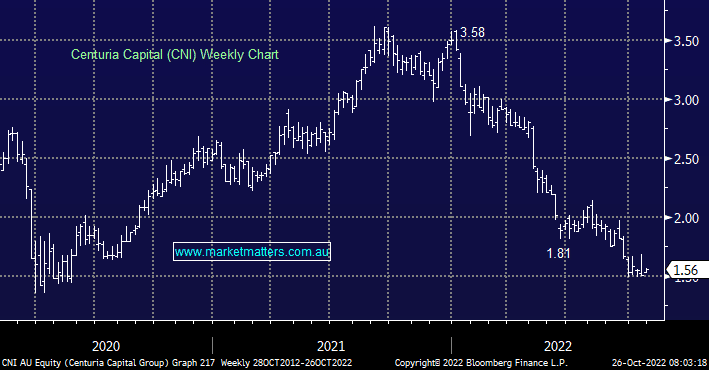

Share prices typically react to new news, outcomes that are not currently factored into the market. Clearly, property has been hit hard over the past year with this property-focused fund manager down 55% YTD, however, what if a ‘less bearish’ outcome prevails? What assumptions have been built into CNI’s current guidance for flat YoY earnings?

- Despite funds under management (FUM) being up 10% on FY22, they have assumed a 10% decline in distributions from their holdings in COF & CIP.

- They assume a more than 30% reduction in transaction activities while performance fees are assumed to be more like $15-20m down from $33m in FY22.

- These in MM’s view are cautious/conservative assumptions that open the door for upside surprises.

MM is high conviction on CNI

Add To Hit List