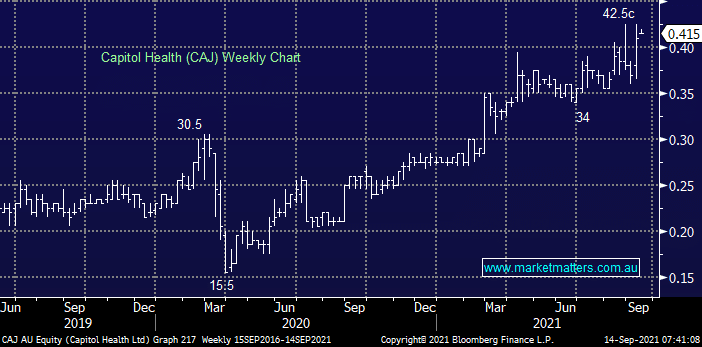

Last week we bought CAJ for our Emerging Companies Portfolio with a couple of reasons front and centre in our rationale:

- Major competitor Integral Diagnostics (IDX) is trading on an almost 2x relative valuation making CAJ very cheap in our opinion.

- Consolidation has already unfolded in the diagnostics space and more appears likely from both trade buyers & private equity.

Hence this is a perfect play for MM as its cheap and has a very real chance of being a takeover target.

MM likes CAJ around 40c

Add To Hit List