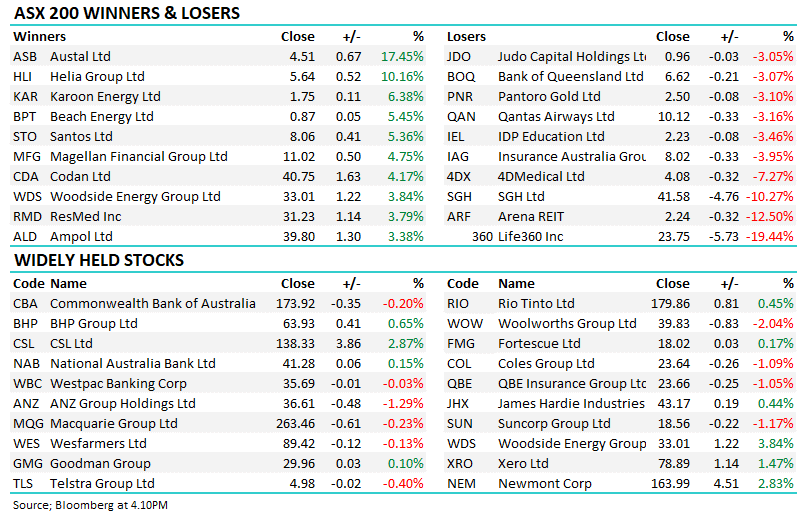

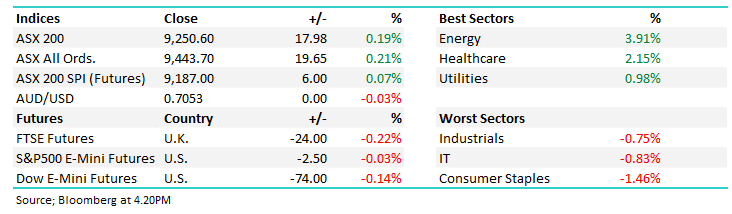

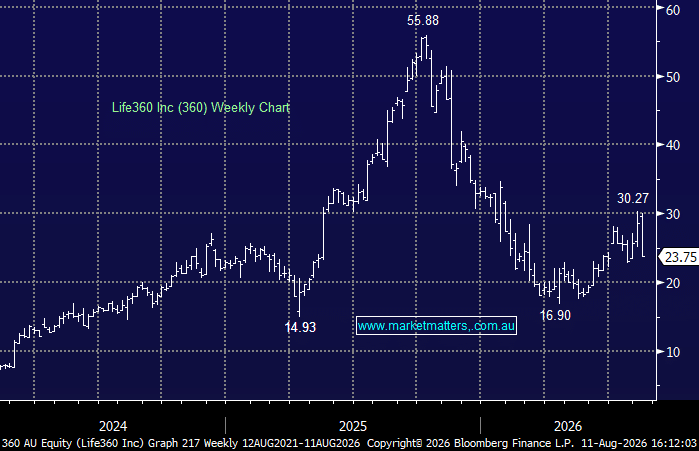

The ASX 200 finished higher today, with the market spending much of the session in positive territory as investors worked through a busy day of reporting season before the RBA took centre stage in the afternoon. The index briefly pushed toward 9,275 following the decision to leave rates unchanged at 4.35%, before giving back some of the move into the close as Governor Michele Bullock made it clear the Board remains a long way from declaring victory over inflation.

The ASX 200 erased some of its late-morning losses on Monday to finish the session down just 0.3%, not a great performance after US indices powered higher on Friday night, with the banks again the local bourse's Achilles' heel. Such was the influence of the banking sector that even though over 55% of the main board closed higher, the index still fell by more than 30 points as a strong resources sector couldn’t offset steep losses by Westpac (WBC) and others.

The ASX eased from near-record highs today as investors turned more selective ahead of a busy week for domestic earnings and monetary policy. Financials were the clear drag after Westpac reported, while strength across materials and gold helped offset some of the weakness.

The US labour market appears to have “rolled over”, with July non-farm payrolls unexpectedly falling by 23,000 and the previous two months revised down by a combined 103,000 jobs. Wage growth also eased to 3.15%, its slowest pace in almost three years, reinforcing the view that inflationary pressures are gradually subsiding. Credit markets responded by scaling back expectations for a September Fed rate hike, with this week's US CPI report now looming as the next key event required to reinforce the less hawkish outlook.

The ASX 200 finished a strong week up +3.2%, posting new highs on three of the five sessions. August is only one full week old, and the local market has already surged towards 9300 with no end in sight as the miners continue to drive the index higher. Monday is set to deliver a repeat performance as a soft US jobs report dulled the prospects of Fed rate hikes, pushing the miners and, in particular, gold names substantially higher after the precious metal surged over US$100.

The ASX 200 finished essentially flat, though it did recover from early weakness, having pulled back and tested this week’s breakout level (~9200), before pushing higher – a positive technical sign. After resetting record highs twice this week, the market moved into more of a holding pattern ahead of next week’s heavier reporting calendar, with strength across materials and technology offset by weakness in the banks and selected healthcare names.

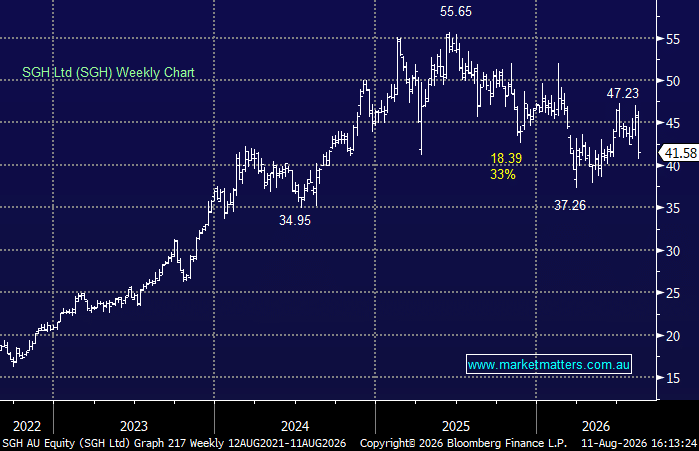

The ASX 200 closed at another record high, briefly trading as high as 9,296 before settling up +44 pts. Materials did the heavy lifting as copper reached fresh records in New York and London, while gold extended its strongest rally in six months. Hopes that a temporary shipping arrangement could restore some traffic through the Strait of Hormuz also continued to support sentiment ahead of the main phase of reporting season next week.

The ASX 200 surged another +0.9% on Wednesday, taking the index well above 9200 for the first time; so much for Liberation Day tariffs, sticky inflation, falling house prices, and the US-Iran War. Gains were broad-based, with more than 75% of the main board advancing as the local market finally punched to new highs; it's only taken 110 trading sessions! A rampant resources market offset weakness in the banks, with BHP on its own contributing 40% of the day's 82-point advance. We don’t want to jinx the local index, but after advancing +5.6% from its intra-day low 9-trading days ago, as we said at the end of July: “We wouldn’t be short for quids.”

Bang! The ASX closed at a fresh record high today at 9,227, with around 75% of the market finishing higher. Some of the more beaten-up areas are also showing signs of life, with software a clear example following better SaaS earnings from the US. Hopes of a lasting peace deal with Iran are also helping sentiment, although we’ll believe that one when we see it.

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

Verication email sent.

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

!

Invalid One Time Password

Please check you entered the correct info, please also note there is a 10minute time limit on the One Time Passcode

To reset your password, enter your email address

A link to create a new password will be sent to the email address you have registered to your account.

Market Matters members receive daily market reports, real-time trade alerts, full access to 5 portfolios and dynamic company data.

Choose how you'd like to proceed:

We have a range of membership options to suit your needs and budget, why not join today and get unlimited access to the premium Market Matters service.