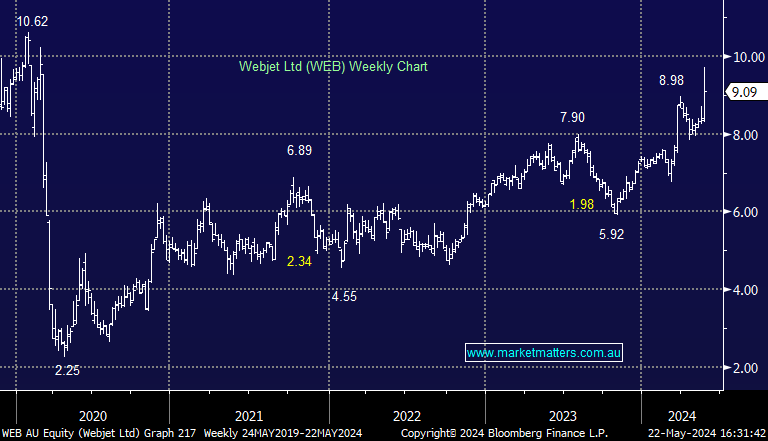

WEB +7.7%: An impressive (but previously flagged) update from WEB today with their FY24 results coming in line with expectations, however, news they are looking to demerge their business 2 business (B2B) division that is growing more strongly from their business 2 consumer (B2C) operation, which has been solid but not spectacular. The concept that a standalone franchise would be more highly valued than the combined entity saw the market bid up the stock.

- On the results front, Revenue of $472m was in line with consensus, EBITDA of $188m was at the top end of guidance ($180-190m) and adjusted net profit of $128m was good.

Their B2B WebBeds business was the standout and growth there looks impressive, with bookings and TTV up ~35%, more than offsetting some weakness in the B2C segment. A demerger would complete in FY25 and we think that would be a major positive.

- All in all, very solid from WEB with a growth catalyst to keep the shares well supported.

MM is bullish WEB

Add To Hit List