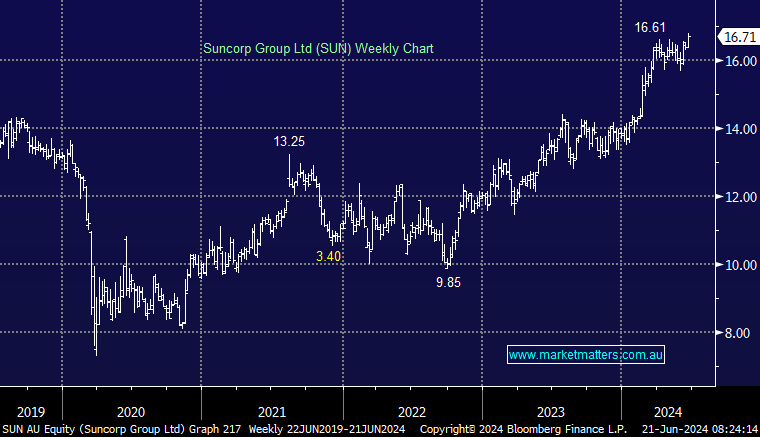

On top of the ANZ deal, in April, SUN announced the sale of its NZ Life business to Resolution Life for NZ$410m. We consider this an attractive move in both strategic and financial terms as it allows SUN to focus on its attractive general insurance (GI) operations. The simplicity of a GI model is appealing to investors and explains the premium trading multiple in IAG relative to SUN, i.e. we prefer the new SUN to IAG moving through FY25. The ANZ and NZ life deals by SUN have come at an opportune time as premium rates continue to improve across most lines of GI business. Looking ahead, we see little reason for the current PE discount in SUN (vs IAG) to persist.

MM is mildly underweight in the financials at this stage, but any dips by SUN due to overall market weakness will cause us to consider SUN seriously to bolster our exposure. An expected dividend yield in excess of 5% moving forward will help patient investors who, like ourselves, are looking for SUN to be revalued further on the upside.

- We like SUN, but the risk/reward isn’t appealing until we see a re-test of $16, or ~6% lower.

MM is bullish SUN into dips

Add To Hit List