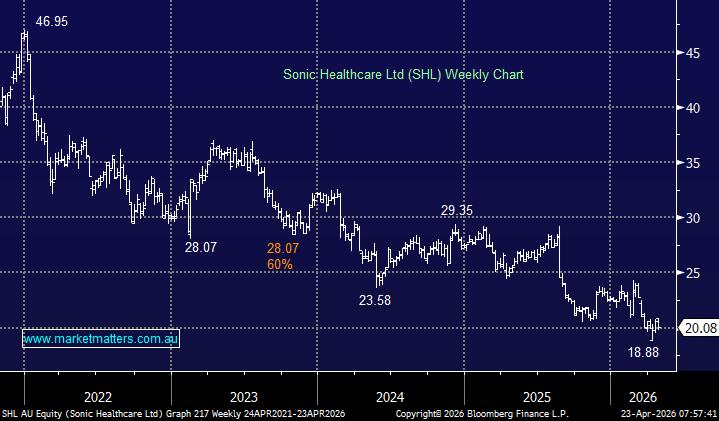

Sonic Healthcare is one of the world’s largest diagnostic healthcare providers, and the leading private pathology operator across Australia, the UK, Germany and Switzerland. It also holds top-tier positions in Belgium, New Zealand and the US with revenue in FY being split Europe (50%), US (25%) and ANZ (25%). While pathology drives the bulk of earnings, Sonic also has a meaningful presence in diagnostic imaging in Australia and is the country’s largest operator of medical centres. If you’ve had a blood test, COVID test, MRI or X-ray through a private provider, there’s a good chance Sonic was involved somewhere in the process.

Sonic is a genuinely world-class business that got artificially inflated by COVID tailwinds, then left holding the bag when they disappeared, all while fighting a structural Medicare pricing war it can’t fully control. The base business is actually growing organically, but nobody cares when the headline profit number keeps falling. Revenue is forecast to grow +18% from $9.6bn in FY25 to $11.3bn in FY27 – the question for investors now is whether the COVID cliff is fully in the base, margins can recover, and the stock — trading well below historical valuation multiples — represents a contrarian opportunity. Given yesterday’s Cochlear news, adding further pressure to the broader healthcare sector sentiment, that conversation just got more complicated.

If, and it’s a big if, we decided to increase our healthcare exposure, SHL is arguably the best option from a risk/reward perspective, although Ramsay also throws up a strong case.

- We like the risk/reward towards Sonic around $20, but caution that this is a contrarian, aggressive view.

MM is cautiously bullish towards SHL around $20

Add To Hit List