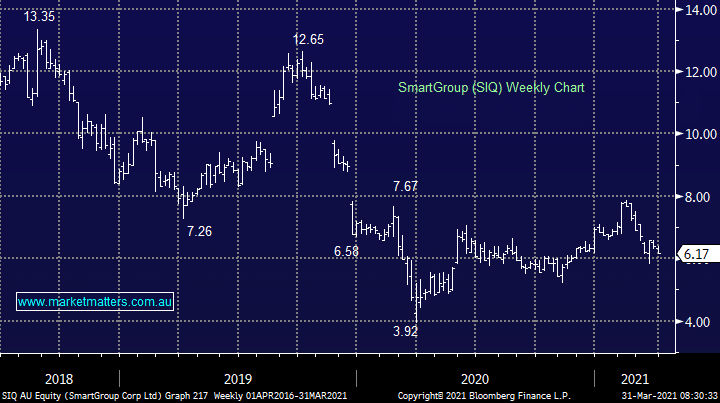

With cash rates so low and income as our primary focus in this portfolio, we want comfort to stay invested, and for that we skew our approach to be more fundamentally driven – to that end, there are few better balance sheets in the portfolio than Smart Group (SIQ).

At the end of FY20 they had a net cash position (i.e. no debt) and that gave them the comfort to pay out a big dividend in March which included a 17.5cps ordinary dividend and a 14.5cps special dividend, both fully franked. That’s a yield of ~5% fully franked for the half alone or 7% grossed for franking, a very strong return in this sort of low rate environment.

The share price has been weak following the March dividend largely due to concerns around the availability of new cars to lease. New car demand has been high and that’s putting pressure on supply. We think this will be a 1H21 issue only with 2H21 looking better.

MM remains bullish SIQ for income

Add To Hit List