One obvious characteristic of BHP’s tilt towards OZL was their understanding of OZ Minerals asset base and how complimentary it is to BHPs existing assets. There are very few hard rock Lithium companies producing and selling Lithium globally, and PLS is certainly one of those with a very good ‘de-risked’ operation.

This is appealing for large cashed up global miners that are prepared to pay more for a greater degree of certainty. We believe that $8.8bn Lithium miner PLS is the quality end of the sector similar to OZL in copper and IGO towards nickel, again we like the stock and perhaps its on RIO’s menu but either way MM believes they are quality, hence our 4% weighting in the Emerging Companies Portfolio.

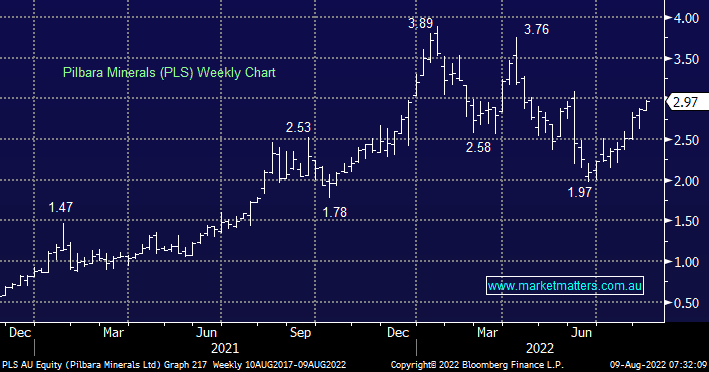

- We currently like this lithium miner and would be a buyer into any pullbacks towards the $2.75 area.

MM remains bullish PLS under $3

Add To Hit List