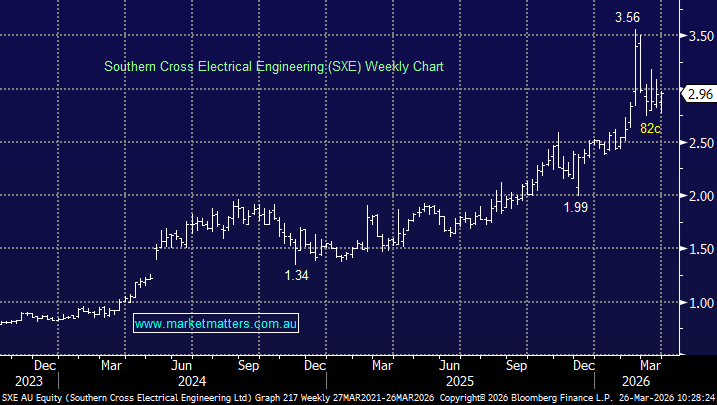

NWH +9.7%: FY24 NPAT was $105.1mn, up 23% $85.6mn a year ago. NRW also produced its highest-ever EBITA result, sending the stock up +9.7%, making it Thursday’s best performer on the ASX200.

- FY Revenue of $2.91bn was up +9.2% from $2.67bn a year ago.

- Revenue for FY25 is projected to be ~$3.1bn with earnings expected to be $205mn to $215mn.

- FY EBITDA of $195.1mn was up 17% year on year.

- NRW Holdings Group Pipeline A$16.4 Billion; A$5.5 Billion Are Active Tenders.

- The construction and mining contractor announced a final dividend of 9c.

Mining contractor NRW recorded stronger-than-expected margins for the year to June 30 and better-than-expected guidance (earnings up about 10 per cent), sending its shares to a 10-year high. NRW is a cyclical stock fund manager’s “trade” based on the earnings cycle. NRW is enjoying a bullish cycle, and UBS analysts think earnings per share will increase by 40% in the next four financial years. However, we are conscious that NWH is trading 25% above its average valuation over the last 5 years as good news gets baked into the share price.

- The strong have largely remained strong throughout 2024, and NRW is no exception. A test of $4 looks likely into Christmas.

MM is cautiously bullish towards NWH ~$3.50

Add To Hit List