In our opinion gold looks fairly cheap both short and longer term which not surprisingly drops down to a sector which is screening very attractively on a valuation basis although its only just started listening to our view. NST have mapped out a 5-year strategic plan following its merger with Saracen (SAR) to produce 2Moz p.a. with declining costs along the journey – sounds good but obviously lots of water to go under this bridge. NST shares have more than halved while gold has retreated less than 20% which is one of the reasons we believe the stock could enjoy some performance catch up extremely quickly and by definition it brings with it an attractive risk / reward profile. The companies financials are solid:

- In the September quarter NST enjoyed sales revenue of $848m and cash earnings of around $170m.

- They are guiding to FY production around 1.6Moz at an all in sustainable cost of $A1,1475-1,5765 (todays price in $A is $2,480).

There are a lot moving parts in the NST share price equation which brings with it risks e.g. bond yields, inflation and the $US are arguably as important as how well NST executes their plans moving into 2022. However, we believe the markets looking at gold and its stocks from a glass half empty perspective hence leaving plenty of room to surprise on the upside.

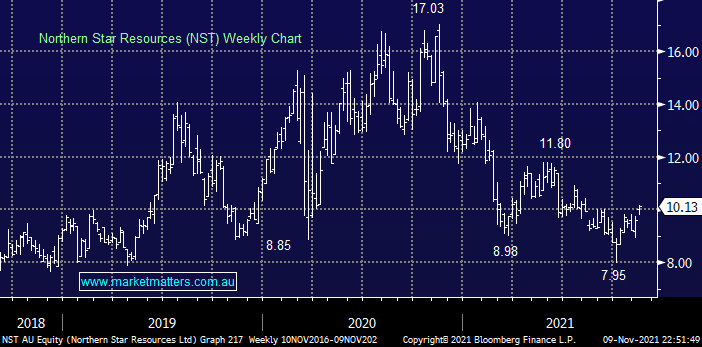

MM likes NST technically if it can hold above $9.70, which delivers exciting risk / reward for an active “play” into Christmas, our consideration is do we want to add to our existing gold exposure (NCM), spread the risks plus lastly the toughest decision is what to sell to fund such a move – thinking caps in place.

MM is bullish NST initially targeting $12

Add To Hit List