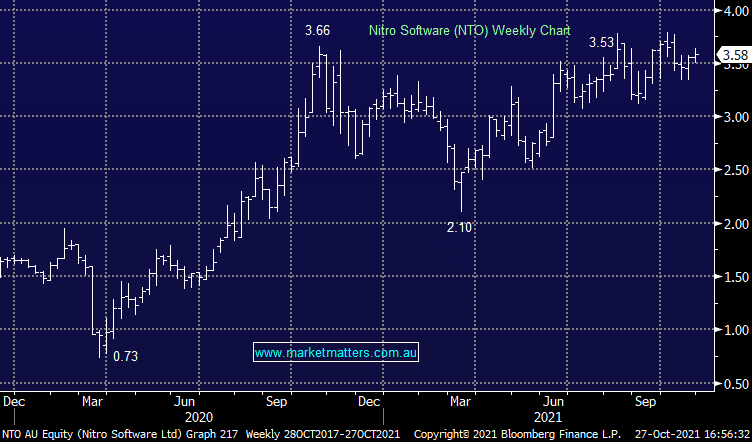

NTO +0.85%: Q3 update from the document productivity company was solid today and came with a small upgrade to guidance for the full year, helping to support the stock on a flat day. Subscription revenue was up 50% year on year, underpinning a 2-4% bump in FY21 revenue guidance to $US49-51m. Expected EBITDA loss was also lowered to under $US10m. The numbers showed Nitro are successfully transitioning sales to a subscription model which now comprises 68% of revenue vs just 56% in Q3 of FY20. A solid update, and in MM’s view with Average Reoccurring Revenue (ARR) growth set to underpin a likely re-rate in the share price given it trades at a steep discount to international peers.

MM remains bullish NTO

Add To Hit List