Hi guys,

The stocks mentioned have been caught up generally in the aggressive sell-off in unprofitable tech, and Australian names have faired worse than their US counterparts, to give some context here, the small-cap software companies on the ASX (which these are a part of) are trading at ~5x EV/Revenue multiples whereas the same cohort of stocks are trading ~9x in the US. One of the main issues is around cash burn, when companies are unprofitable, they rely on the support of capital markets to keep them afloat. Capital markets have turned negative on tech and specifically so on names that are burning cash.

That said, these 4 companies are good operators, growing strongly into large markets and are simply out of favor right now. I have rated our views on each in the context of the group.

Whisper (WSP): Reported well recently and signs a turnaround of fortune is building. They have a strong core in ANZ with growth in Asia the upside. We rate WSP 3/4 listed here.

Dubber (DUB): We caught up with management this week, they have net cash ($108m) and no requirement to raise in our view. The key metric here to care about is annual reoccurring revenue (ARR) and it continues to climb. We like DUB here rating it 2/4.

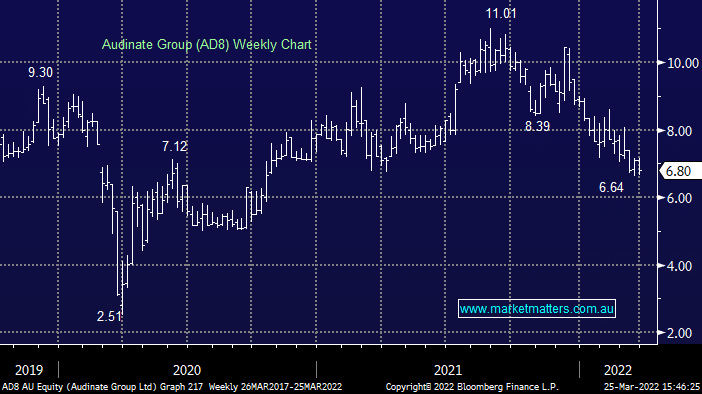

Audinate (AD8): This is a quality operator, dominate market position, reopening trade and on this list it would be rated 1/4. Lower risk than the others.

Nitro (NTO): The global leader in their space DocuSign (DOCU US) has had major issues and fallen by 2/3rds. While we still like NTO and will continue to hold, we rate this as our least preferred of the 4, and we will likely cut into strength.