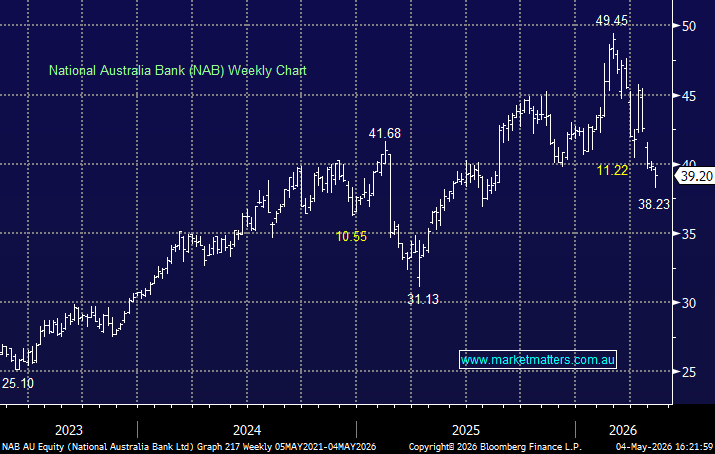

NAB –1.58%: fell after a softer 1H result, with cash profit missing expectations as higher costs and weaker revenue weighed on the outcome.

- Cash profit: $2.64bn vs $3.0bn est.

- Net interest margin: 1.81% vs 1.77% est.

- Cost-to-income ratio: 59.1% vs 48.9% y/y

- ROE: 8.5% vs 11.7% y/y

- CET1 ratio: 11.7%

The miss was largely revenue-driven, though the bigger concern was a sharp increase in costs, partly reflecting software capitalisation changes and ongoing investment spend. While bad debts rose, overall asset quality remains sound, with early arrears still trending lower.

There were some positives under the hood, with Business & Private Banking (+12%) and Personal Banking (+26%) showing solid profit growth, while margins improved slightly. Management is targeting >$450m in productivity savings in FY26, with cost growth expected to moderate from here.

The result was messy given changes to capitalization of software costs, but okay. The key will be whether NAB can deliver on cost control and stabilise revenue trends into the second half.

MM is neutral NAB, preferring ANZ & WBC

Add To Hit List