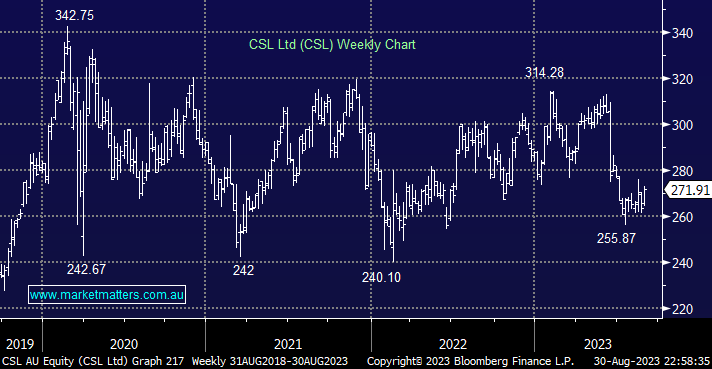

At MM we thought CSL’s report was ok this month with revenue growth guidance of 9-11% above consensus but the market’s reaction has been muted at best. We can see this stock re-rate back on the upside over the coming months supported by its position as a growth-oriented large cap pharma, especially as we see little near-term downside risk i.e. were keen buyers into dips under $260.

- We like the risk/reward toward CSL ~$270 as yields and the $A drift lower.

MM is considering CSL into recent weakness

Add To Hit List