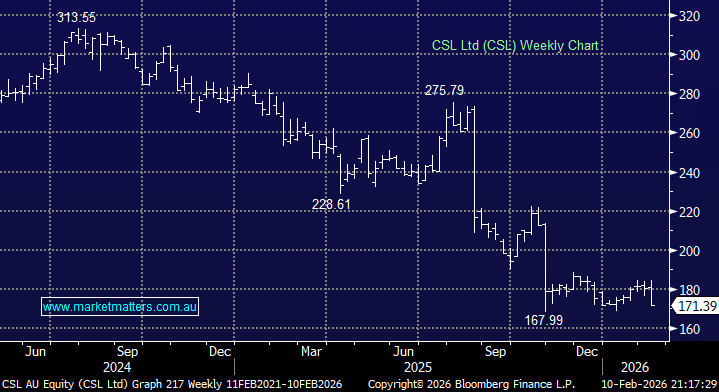

CSL captured the headlines for all of the wrong reasons yesterday as they announced the abrupt departure of CEO Paul McKenzie ahead of this morning’s 1H26 results – which are pretty much in line with expectations at the headline level, but some weakness in composition and they have a lot of work to do in the 2H.

1H26 Highlights:

- 1H revenue $8.3bn v estimated $8.46bn.

- NPAT (adjusted) $1.95bn v $2.07 YoY, but pretty much inline with $1.96bn expected

- Share buy back expanded from $US500mn to $US750mn.

- Dividend $1.30m v estimated $1.33.

They maintained their FY26 guidance which is for adjusted earnings (NPATA) to be up 4-7% for the year, with the market (consensus) currently at +5.5%, though they clearly have a lot of work to do in the 2H to achieve that result, and we suspect they’ll be some caution given the abrupt change of leadership. Ultimately, we suspect some weakness early today, and then it will be up to how well the message is articulated on the earnings call– it will be an interesting one!

- We feel any knee-jerk sell-off following this result will deliver a solid risk/reward opportunity considering the stock’s current relatively discounted valuation.

MM remains long and cautiously bullish on CSL around $170

Add To Hit List