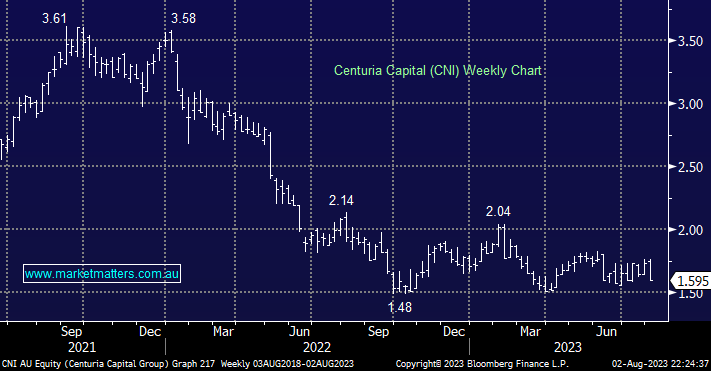

Industrial real estate manager Centuria Capital should be a significant beneficiary of falling bond yields as they carry a fairly low level of hedging but the sector is under pressure as valuation write-downs come through thick and fast, often realty checks like these can provide opportunity. We believe declines in asset values have already been factored into the CNI around current levels, and their large holdings in Centuria Office REIT (COF) and Centuria Industrial REIT (CIP) could support performance after detracting from it over the past 12 months as interest rates tore higher. CNI is currently forecast to yield 7.2% over the next 12 -months which should help the patient investor.

- We are considering CNI for our Flagship Growth Portfolio into market/sector weakness under $1.50.

MM remains long and bullish CNI in two portfolios

Add To Hit List