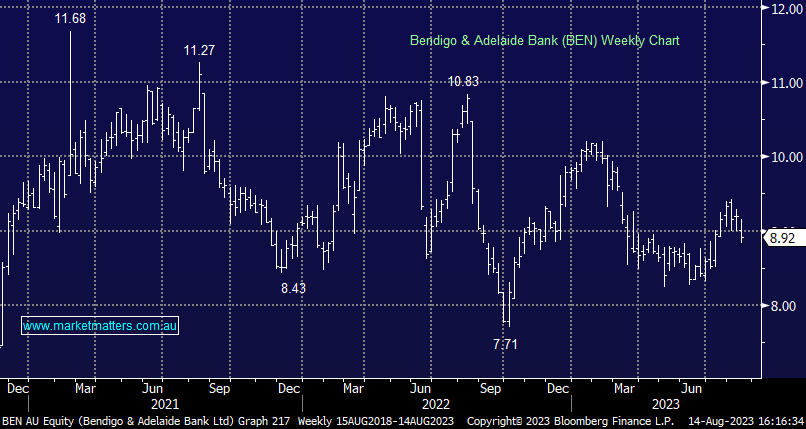

BEN -2.94% A miss at the earnings line drove a decline in the share price today, although it wasn’t all bad news for this regional lender. Cash net profit after tax (NPAT) of $282m was a ~5% miss to the $299m expected while the FY23 dividend of 61cps was around 1% ahead of consensus. Their capital position was solid while impairments of $28m were also as expected – and low given our point in the cycle. They did better in the 2H with net interest income (NII) of $843m ~4% ahead, underpinning better net interest margins (NIM) which increased 8bps to 1.94% – a return to loan growth + better NIMs HoH (despite -5bps in Q4) are the key positives to take away from the result. Asset quality, as was the case with CBA, remained sound despite all the doom and gloom.

- An earnings miss but some signs of improvement more broadly – not a bad update overall.

MM remains neutral on BEN ~$9.00

Add To Hit List